Executive Summary

This will be the year when the regulation of platform companies starts to bite following growing concern about misinformation, privacy, and market power. Something once considered unthinkable has become ‘inevitable’, in the words of Apple boss Tim Cook – though the details will be messy, hard-fought, and take time to play out. Meanwhile the spread of false, misleading and extreme content will continue to undermine democracies around the world with polarising elections in India, Indonesia and Europe likely flashpoints. Journalism will continue to be hollowed out by structural shifts that have already led to significant falls in advertising revenue. Publishers are looking to subscriptions to make up the difference but the limits of this are likely to become apparent in 2019. Taken together these trends are likely to lead to the biggest wave of journalistic lay-offs in years – weakening further the ability of publishers to hold populist politicians and powerful business leaders to account.

It is a crucial year [in which] social media platforms have to prove they care about the truth and about paying for serious journalism, or be properly forced to do both by regulation.

It is a crucial year [in which] social media platforms have to prove they care about the truth and about paying for serious journalism, or be properly forced to do both by regulation.

It is a crucial year [in which] social media platforms have to prove they care about the truth and about paying for serious journalism, or be properly forced to do both by regulation.Ben De Pear, Editor, Channel4 News, UK

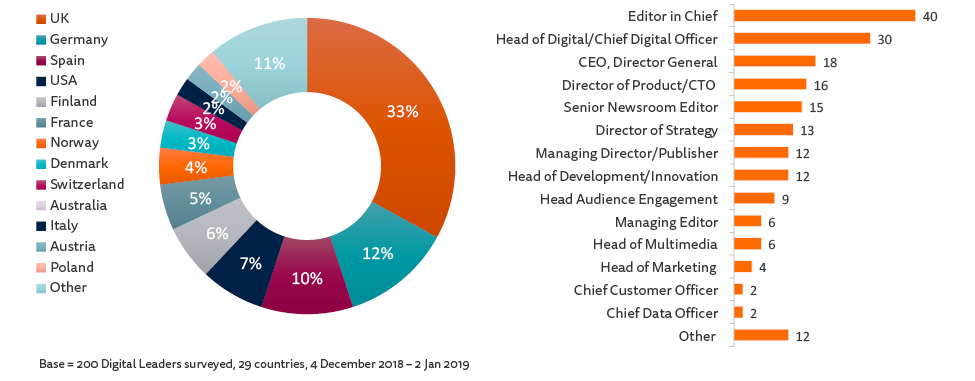

In our survey of 200 editors, CEOs, and digital leaders:

- Subscription and membership is the key priority for the news industry going forward. Over half (52%) expect this to be the MAIN revenue focus in 2019, compared with just 27% for display advertising, 8% for native advertising and 7% for donations. This is a huge change of focus for the industry.

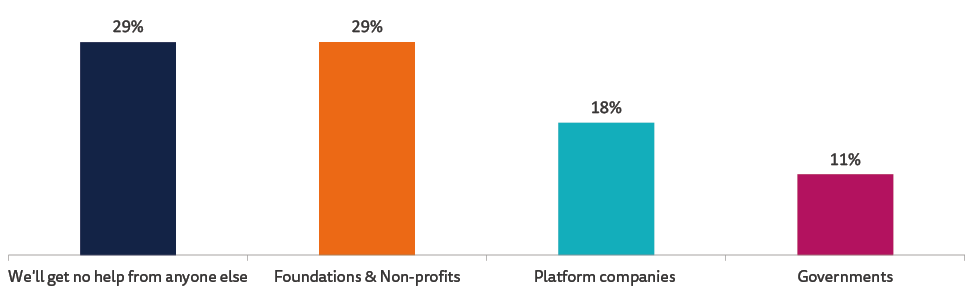

- At the same time, there seems to be a growing acceptance that some types of quality news provision might need to be subsidised. Almost a third (29%) expect to see significant help this year from foundations and non-profits, a fifth (18%) expect tech platforms to contribute more, while one in ten (11%) think governments will provide more support. A further 29% of publisher respondents is not expecting any of the above to ride to their rescue.

- The news industry is losing patience with Facebook and publishers are re-focusing attention elsewhere. Less than half of respondents (43%) say the platform is likely to be important or extremely important this year, a similar number to Apple News and YouTube – but far less than for Google (87%).

- Almost two thirds (61%) are concerned or extremely concerned about staff burnout. Retaining (73%) and attracting (74%) staff is a particular headache, given the low rates of pay, relentless pace and pressures of a modern newsroom. Over half (56%) are concerned about levels of newsroom diversity.

- Over three-quarters (78%) think it is important to invest more in Artificial Intelligence (AI) to help secure the future of journalism – but not as an alternative to employing more editors. Most see increased personalisation as a critical pathway to the future (73%).

- With many publishers launching new daily news podcasts, it is perhaps not surprising that the majority (75%) think that audio will become a more important part of their content and commercial strategies. A similar proportion (78%) think that emerging voice-activated technologies, like Amazon Alexa and Google Assistant will have a significant impact on how audiences access content over the next few years.

I’m surprised about the potential of audio and voice for journalism. Users will consume news by speaking and listening, less often by reading — and we have to prepare early on for […] shifts in user expectations.

I’m surprised about the potential of audio and voice for journalism. Users will consume news by speaking and listening, less often by reading — and we have to prepare early on for […] shifts in user expectations.

I’m surprised about the potential of audio and voice for journalism. Users will consume news by speaking and listening, less often by reading — and we have to prepare early on for […] shifts in user expectations.Stefan Ottlitz, Der Spiegel

More Specific Predictions

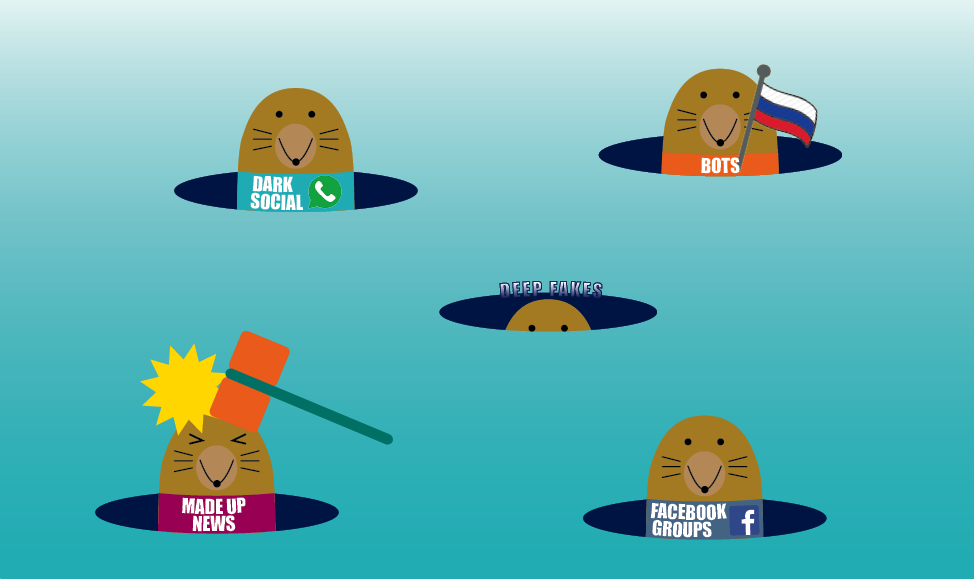

- Platforms step up their battle against misinformation and disinformation but the problem shifts this year to closed networks and community groups, where it is harder to track and control.

- We’ll see a renewed focus on trust indicators for news and better labelling designed to help consumers decide what and who to trust.

- With consumers increasingly conscious of the time they are wasting online, we’ll see more people leaving social networks, more tools for digital detox, and more focus on ‘meaningful’ content.

- Slow news becomes a theme with the launch of new journalistic enterprises like Tortoise (UK) and the Dutch De Correspondent expanding to the US. These are billed as an antidote to the current glut of quick, shallow, and reactive coverage. But how many will join – and pay?

- The rise of paywalls is shutting more people off from quality news and making the internet harder to navigate. Consumer irritation will build this year, leading to a combination of more news avoidance and the adoption of ‘paywall-blocking’ software.

And in technology …

Watch out for foldable phones and 5G capable handsets. We’ll see the first commercial driverless ride-sharing services and hear more about the potential of the blockchain for journalism.

News start ups to watch include Kinzen and Curio.

1. Looking Back at 2018

This was a year of ‘techlash’ – where the media and political narrative turned against big Silicon Valley platforms. These giant companies are increasingly portrayed as omnipotent, anti-competitive, and not facing up to their wider responsibilities to society – even if individual platforms carry very different level of public trust.1 Far from championing democracy they are seen as undermining it. Instead of protecting our privacy, they are accused of playing fast and loose with it. Ideals about time well spent have been replaced by concerns about addiction and the impact on our mental health.

In particular it was an ‘Annus Horribilis’ for Facebook and its founder Mark Zuckerberg who were hit by a succession of PR crises from the Cambridge Analytica data leaks, to misleading advertisers and publishers over video data, and the continued spread of damaging rumours, half-truths and hate speech across the world.

In the spotlight: Mark Zuckerberg faces Congress and the media

Facebook CEO Mark Zuckerberg arrives to testify before a Senate Judiciary and Commerce Committees joint hearing regarding the company’s use and protection of user data, on Capitol Hill in Washington, U.S., April 10, 2018. REUTERS/Leah Millis

We didn’t focus enough on preventing abuse and thinking through how people could use these tools to do harm as well.

Mark Zuckerberg

At the beginning of the year Mark Zuckerberg pledged to ‘fix Facebook’ and a huge amount of engineering resource has been deployed, fact-checking and media literacy programmes have been funded, along with support for local journalism in some countries.2 Facebook, Twitter, and YouTube have all spent increasing amounts of money on taking down content and targeting ‘bad actors’ and even extending the definition of unacceptable content. In this respect, the banning of Info-Wars, first by Apple and then by other platforms marked a major shift in approach3. But the scale and complexity of the task ahead is immense.

Every week new problems emerge – a bit like a game of ‘whack-a-mole’. By July the crisis spread to WhatsApp with false rumours about child abduction in India leading to a series of lynchings4. In Brazil, a co-ordinated disinformation campaign on WhatsApp played a part in the rise to power of far-right leader, Jair Bolsonaro5. And by the end of the year attention had switched back to Facebook, where hundreds of self-organising ‘anger groups’ laid out their demands and organised destructive ‘Gilets Jaune’ protests across France.

Social media was once seen as an enabler of free information, helping citizens to break free from elite gatekeepers like journalists. This may still be true in developed societies where the media is still relatively strong, but events of the last year have shown how different the situation can be in countries like India, the Philippines, Myanmar and Brazil. When just a handful of apps provide the main way in which most people access and share information, the risks of misinformation and manipulation increase exponentially. It should be added that much of the manipulation is carried out by domestic political elites running organised, large-scale, and well-funded campaigns.

Last year, we correctly predicted that platform efforts to damp down fake news would lead to accusations of censorship. In France ‘Gilets Jaune’ protesters talked about suing Facebook for deliberate suppression of their views6 – at the same time as their opponents blamed incendiary algorithms for fomenting unrest. Donald Trump says Facebook, Google and Twitter are intentionally and illegitimately suppressing conservative viewpoints while liberals accuse them of promoting extreme viewpoints. Damned if they do and damned if they don’t, platforms are no longer seen as neutral7, condemned to become political footballs through this year and beyond.

Accepting the extent of our digital addiction

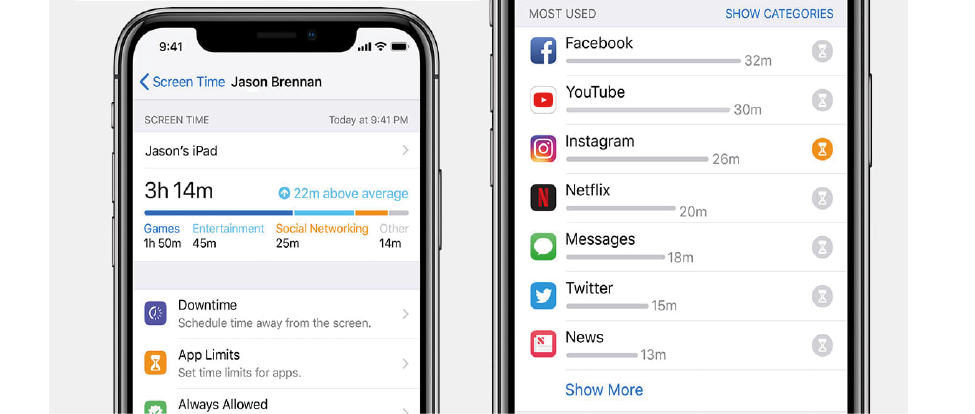

Reports about the harmful impact of the internet led to something of an existential crisis in Silicon Valley in 2018. Engineers and former engineers are having second thoughts about the ethics of ‘designing for addiction’, using notifications that are dripping with dopamine, or surfacing content that pushes us apart. Algorithms have being reprogrammed and metrics reset, while the ‘time well spent’ mantra of former Googler Tristan Harris has truly taken hold. With Apple’s iOS 12 update and the introduction of the ‘screen time feature’, we can now see how much time we spend with our phone, how many pick ups we take each day. By implication we start to see what or who else might be losing out.

Apple screen time feature launched in June

In some ways this can be seen as an assault by Apple on its key rivals – it is no co-incidence that Facebook, You Tube and Twitter are amongst the apps consuming most attention – but this has also tapped into genuine consumer concerns about wasting time and what technology is doing to us. Expect more press articles about ‘digital well-being’, more pressure to delete our social media accounts, and more software and dashboards to help control our addiction.

News media ups and downs

Reducing ‘time spent’ is a challenging concept for under pressure media companies, especially those that are mainly funded by advertising. In January Facebook announced it would show less publisher content in the news feed in favour of ‘meaningful interactions’. Little Things, which built its business on sharing inspirational stories about humans and pets, was the first casualty after its organic reach dropped 75%, while other traditional publishers reported falls of 20% or more. Mail Online lost almost 2m users8, while Verizon wrote off around $4.6billion of its media investment in Oath (which includes AOL and Yahoo) after lower than expected revenues.

Companies that had become overly dependent on Facebook pivoted or downsized. BuzzFeed made redundancies in the UK and closed its French operation. Vox media cut around 50 jobs mainly focused on social video. Mic.com laid off most of its staff and was sold for $5m, a fraction of its previous value, after what CJR termed ‘management hubris’ and a disastrous pivot to video.9

Traditional publishers have also been feeling the pinch, especially local and regional ones. In the UK Johnston Press, publisher of the ‘i’, the Scotsman and the Yorkshire Post, collapsed – only to be reborn as JPI media, free of much of its huge debt and historic pension obligations. In Canada six more local newspapers closed. Public service broadcasters such as ABC, DR and the BBC face huge cuts and further upheaval as a result of shifting consumption patterns and pressure from politicians.

Advertising is in trouble – long live subscription (and donations)

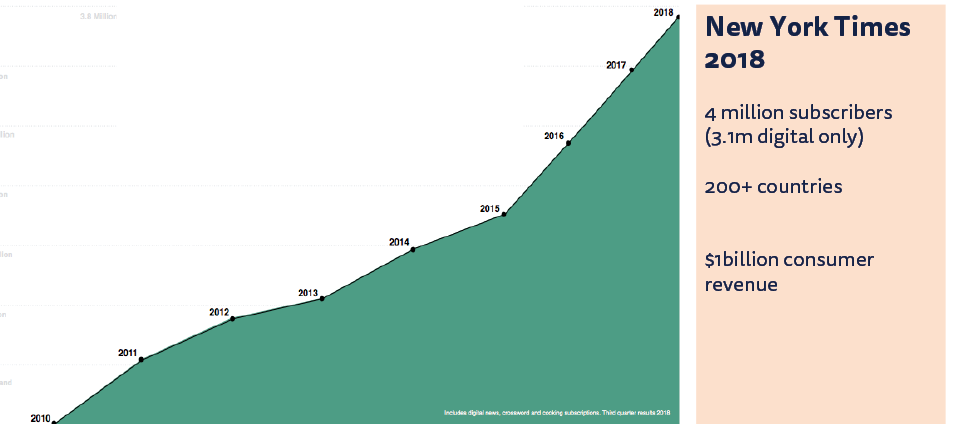

On the plus side, some publishers that have re-focused on ‘reader payment’ are thriving. The New York Times is now running at four million subscribers (3.1m digital) with a mantra that every piece of content should be worth paying for.

New York Times subscription growth 2010-18

Source: New York Times

Nordic publishers are also at the forefront of digital subscription trends.10 Sweden’s divisive elections helped Dagens Nyheter to top 150,000 digital subscribers for the first time while in Finland Helsingin Sanomat returned to growth off the back of sharp rises in digital subscription. And in France, Mediapart celebrated its tenth year with profits of €2.4m off a subscription base of 140,000. It seems that investigative journalism can thrive in a digital age and make money too.

But 2018 was also a year when membership and donation models took hold. The Guardian announced one million ‘supporters’ over the last three years (via donation or membership) and are on the verge of breaking even, after years of heavy losses. This is an alternative vision of reader payment that ensures the widest possible access to scoops like Cambridge Analytica11 and the Windrush Scandal.12

New models, old skills

One consequence of the shift in business models is the focus on developing loyalty and retention, which is why newsletters are making a comeback, with more publishers reclaiming them from marketing teams. One new trend for 2018 was the development of pop-up newsletters, designed to drive episodic engagement. CBC ran an eight week series on the Royal wedding called the Royal Fascinator. Politico experimented with an eight week series of explainers and tools aimed at educating younger voters. The format engaged over 8,000 people with open rates of over 55%.

Pop-up newsletters – with a podcast sensibility

Optimising for Google has also been another ‘back to the future’ trend for 2018 with publishers noting a bigger proportion of their traffic now coming from news search and AMP pages in 2018, as well as from the new tab on Chrome browsers, which now displays personalised news sites. Search Engine Optimisation (SEO) skills will become ever more important in 2019 following Google’s decision to put a news feed (called Discover) on the main search page of all mobile browser for the first time. This will roll out gradually but will have a significant impact on news referrals.13

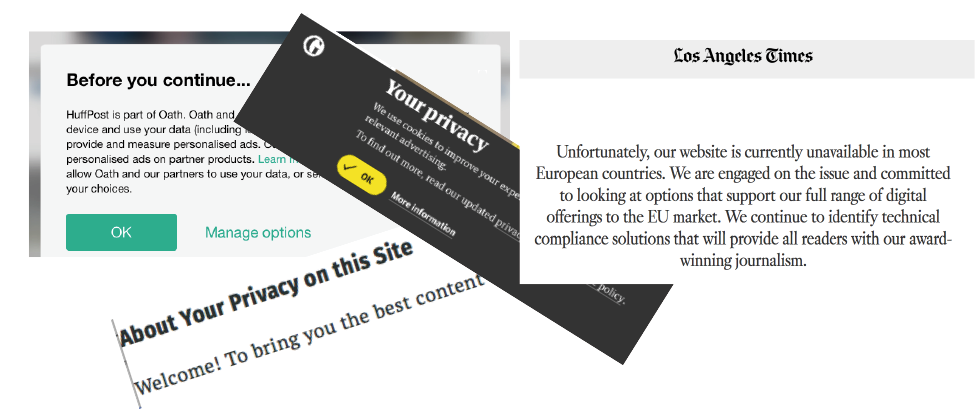

GDPR – was it worth all the fuss?

This time last year, media companies were stressing out about the impact of new European privacy legislation on businesses. So did GDPR clean up the worst excesses of ad tech and give consumers back control of their data? Not exactly …

GDPR has led to bigger, complex privacy notices, and more digital clutter

GDPR forced publishers to clean up their permissions and processes (a good thing), but the wider benefits are harder to see. In practice, the messages and overlays were too confusing and complex for most people to engage with, so the majority just ticked ‘yes to all’. So unwanted emails continue, third party cookies continue to be served14 and consumers are still routinely targeted across the web programmatically. One unexpected side-effect was that GDPR also broke the internet with more than 1,000 US publishers, including the Los Angeles Times, choosing to block European readers rather than face the risk of massive fines. Nine months on, most publishers report little impact on their bottom line (even though many spent significant sums preparing for the new regulation).

GDPR implementation may be done and dusted but the core issues around privacy won’t go away and better and more imaginative solutions will be needed in the future. Now all eyes are on the US where a similar privacy proposal is in play.

Technology as an enabler for better journalism

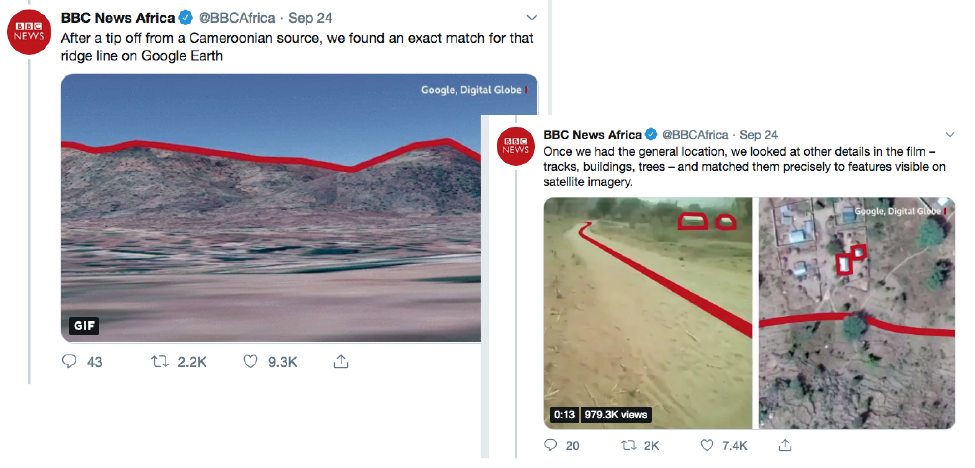

The past year has also shown how technology can help journalists uncover truth – something we’ve highlighted in previous predictions reports. Perhaps the best example came from BBC Africa Eye’s investigation into the killing of women and children in Cameroon. The team used open-source technology, collaborative human networks, combined with tools like Google Earth to show where and when the atrocity took place – and to finger the likely culprits. The resulting TV programme and twitter thread15 will deservedly win awards this year.

BBC Africa Eye: Anatomy of a Killing

Similar technological and collaborative approaches have inspired Bureau Local, which does the heavy lifting around data sets on behalf of a range of local news partners in the UK. The network has broken more than 30 exclusive stories, including an investigation into council finances, which revealed that half of the councils in England planned to cut children’s services.

Throughout 2018 we’ve seen some of the worst of social and digital technology, but also how they can be harnessed to deliver better and more impactful journalism. With new technologies such as Artificial Intelligence on the way, that can give us some hope going into the next year.

2. Key Trends and Predictions for 2019

In this section we explore key themes for the year ahead, integrating data and comments from our publishers’ survey. For each theme we lay out a few suggestions about what might happen next.

2.1 Platforms under pressure

2.1.1 Information Disorder Spreads to Closed Networks, Platforms Struggle to Restore Reputation

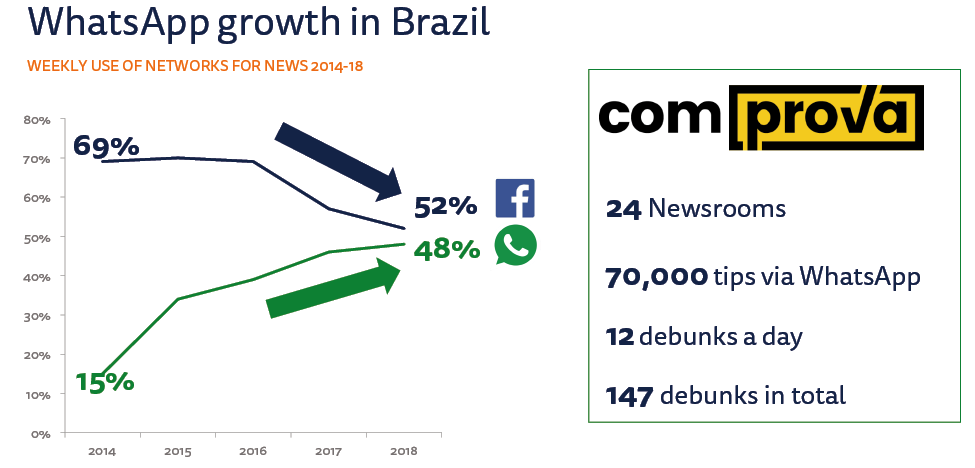

Our Reuters Institute Digital News Report has tracked the growing importance of WhatsApp and other messaging platforms particularly in developing countries (see chart below). Around 120m people use WhatsApp in Brazil and with politics deeply polarised this closed network has increasingly turned into a political battlefield. The Brazilian elections were something of a test case for whether it is possible to track and debunk misleading information in WhatsApp.

WhatsApp has become key network for information and disinformation in Brazil

Reuters Institute Digital News Report 2014-18, Q12b. Which, if any, of the following have you used in the last week for news? Base: Approx 2000 each year. (Urban sample)

The Comprova project, an alliance of 24 newsrooms, started a WhatsApp ‘tip line’ where ordinary people could send information to be checked. At its peak it was dealing with 2,000 messages a day, but the project could only check a fraction of those. In total it managed to check 147 successful debunks – an impressive task but just a drop in the ocean compared with the scale of the problem.

Claire Wardle, who runs First Draft which supported the Comprova project, as well as others around the world, says the nature of problem has changed. Misinformation is no longer about completely false news, but rather a constant drip, drip, drip of ‘misleading content designed to deepen divisions in society’. In this context, she argues, newsrooms may need to change their approach this year.16

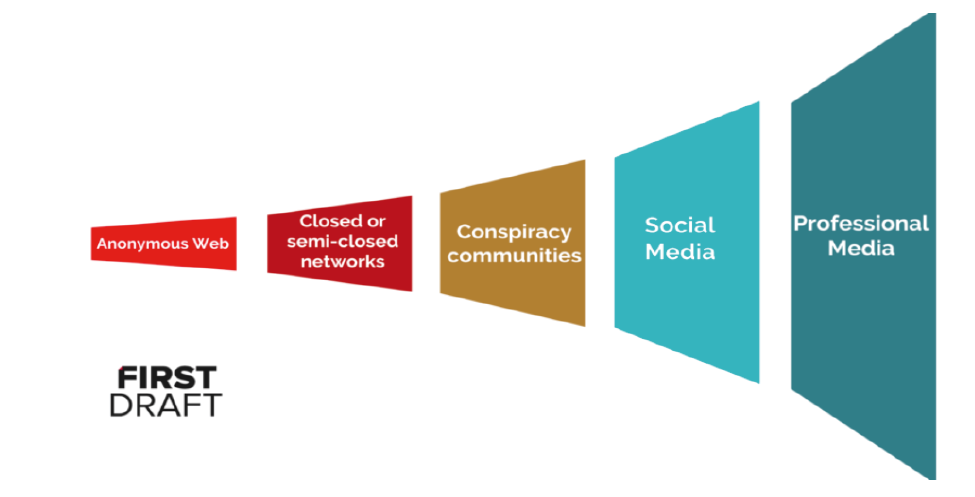

Fact-checking and debunking may need to be supplemented by a greater understanding of how stories are spread and by whom. First Draft research shows that misleading content is often discussed first in the anonymous web (4chan and Discord), then co-ordinated in closed or semi-closed networks (WhatsApp or Facebook groups), is then socialised in conspiracy communities (Reddit forums, YouTube channels), before being seeded in a co-ordinated way in public networks like Facebook, Twitter and Instagram. Broadcast media and newspapers can then often make the problem worse by picking up and amplifying these claims. In September, social media scholar dana boyd warned that the media are being ‘played’ and need to be more aware of the role they can play in giving credence to unfounded claims (e.g. that the Parkland students were ‘crisis actors’).17

Amplification trumpet: how misleading ideas get spread …

Platform approaches are developing fast …

Facebook has deployed advanced technology as well as increased human resources to identify and remove fake accounts. It has tightened up rules on political and ‘issue-based’ advertising with new requirements for authentication and clarity about the affiliation of those taking out ads. It has continued to work with fact-checkers to identify problematic content, claiming that the visibility of identified content has reduced by 80%.18 At the same time it has boosted the prominence of ‘trusted news sources’ in its algorithms, based on surveys of Facebook users. Overall, the impact of these changes is hard to assess though a study from the University of Michigan suggests significantly reduced engagement levels with unreliable sites in the US since 2017.19 A French study suggests engagement with ‘dubious’ sites has halved in France since 2015.20 The company has helped fund wider initiatives such as the News Literacy Project and the News Integrity project.

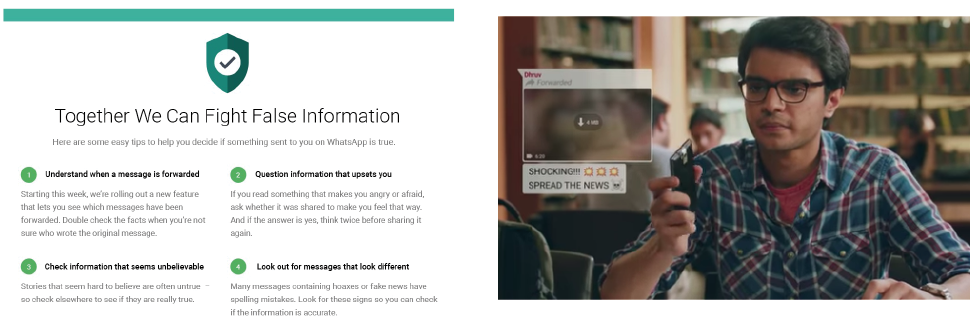

WhatsApp has tried to reduce the virality of false news by imposing limits on forwarding from 250 people to a maximum of 20. In India the limits are even tighter while a ‘quick forward’ button next to media messages has been removed. Full-page newspaper and TV spots were taken out in India to warn of the dangers of sharing fake news21. Expect a ramping up of this activity ahead of elections this year.

Press and TV campaigns in India on the dangers of sharing false news

YouTube has implemented new measures to counter conspiracy videos and false news. Trusted news sources are now prioritised around breaking news, while it plans to add more contextual information on news sourcing and around historic conspiracy theories like the ‘fake moon landings’. YouTube is also attacking economic incentives by marking problematic videos un-monetisable and enlisting prominent YouTubers to help with digital literacy.

Twitter has clamped down on fake accounts and introduced new ways of identifying bots impersonating humans. Twitter now challenges around 9m accounts a week that it suspects could be automated to prove that there is a human behind them. In the US mid-term elections it removed over 10,000 accounts and introduced a new labelling system for official candidates.

I think we’ll learn in 2019 whether platforms are serious in their attempts to combat misinformation or work with news organizations to more clearly label trusted sources. I’d like to believe they are, and the teams they have working on these issues are coming at them conscientiously. It’ll take real resourcing to give these efforts teeth.

Senior leader at a top US publisher

What Might Happen in 2019

Election flashpoints: Polls this year in India and Indonesia will be key tests of social media’s new defences. The Indonesian government has set up a war room of 70 engineers22 and has threatened to block Facebook entirely if things get out of hand. Meanwhile in India a rise of intolerance and religious hatred has coincided with the rapid growth of social media. Political parties and other activists have set up thousands of WhatsApp groups in order to spread messages, many of which will be hard to monitor openly. A recent BBC study suggested that many Indians feel as though they had a patriotic duty to forward information and that the validation of belief systems often ‘trumps the verification of the facts’.23

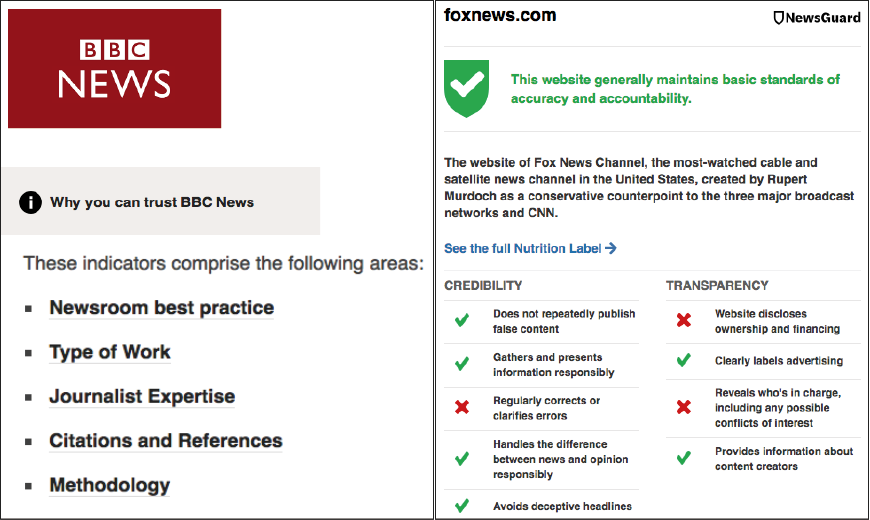

Nutrition labels for news: Social and search platforms as well as other aggregators will place increasing focus in 2019 on the credibility and track record of a publisher when making decisions on what to show. This has already proved one of the most effective ways of down-ranking false news, but this year we may start to see more systematic approaches gaining traction. Around 120 news sites have started to display trust indicators on their pages, with links to detailed policies on ethics, fact-checking and corrections. It is hoped that these will provide some objective standards to separate reputable news sites from unreliable ones.

Trust Indicators for BBC News | Newsguard assessment of Fox News

Newsguard is a new venture that aims to rate (as green or red) every significant site in the United States. It also provides a more detailed ‘nutrition label’ write-up on 4,500 English language websites. These labels are created by a human researcher and to that extent are open to biases. This process is likely to be controversial not least because many sites rated as ‘unreliable’ are on the political right. Breitbart, for example, is labelled red because it ‘sometimes distorts or omits facts to fit its agenda’. On the other hand, Fox News has been assessed as maintaining ‘basic standards of accuracy’ (green), even if the more detailed label criticises aspects of its performance in not correcting errors.

Expect to see more labelling initiatives in 2019, though they will inevitably be subject to partisan attack and may struggle to scale and keep up-to-date. Platforms are pursuing their own media rating initiatives and will be looking for solutions that scale across countries and languages.

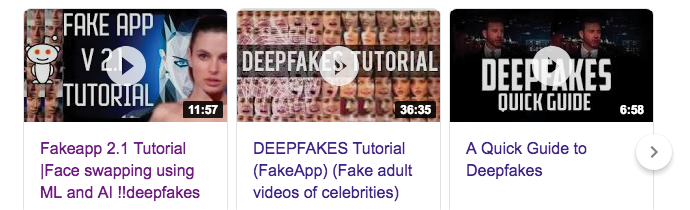

Deep fakes: With sophisticated video manipulation technology now openly available many fear a new wave of misinformation. Software such as Fake App has made the technology easy to apply for those with basic programming skills – not least with free tutorials readily available on YouTube. A video of Barack Obama calling Trump a ‘total and complete dipshit’, was released in April by film director Jordan Peele in conjunction with BuzzFeed as a way of raising awareness about how AI-generated synthetic media could be used to distort and manipulate reality. Deep fakes have also been widely used to insert celebrities into pornography and to add the actor Nicolas Cage into movie scenes. Expect a proliferation of deep fakes in 2019 including the first attempts to deploy these powerful technologies to literally put words into the mouths of political opponents.

Tutorials for deep fakes are widely available online

Overall, we can expect new threats to emerge as fast as old problems get fixed. Removing or demoting unreliable sources, raising digital literacy, improving journalistic standards and better labelling will all help but lasting solutions will require platforms, publishers and governments to work together for years to come.

2.1.2 Publishers Look to Wean Themselves Off Facebook

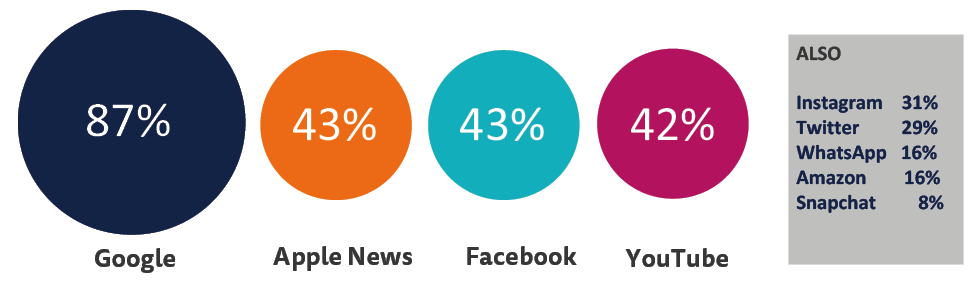

Our digital leaders survey shows publishers looking to diversify away from Facebook and towards other platforms this year. Google remains the key priority for most, with more than eight in ten (87%) saying it will be ‘very’ or ‘extremely important’, but publishers are also looking again at YouTube, Instagram and Twitter as they look to reach new audiences.

Interestingly, Apple News (43%) is now considered as important as Facebook, with some publishers reporting sharp increases in traffic. Slate’s page views via Apple News doubled in the first half of 2018, with Vice showing similar leaps and Mother Jones reporting traffic increases of 400%. Despite this, most traffic remains trapped in an Apple controlled environment and advertising revenue remains limited.24

How publishers rate platforms going into 2019

% saying each platform was ‘very’ or ‘extremely’ important

% saying each platform was ‘very’ or ‘extremely’ important

Q1. How important do you expect the following platforms to be for your news organisation in 2019? Digital leaders survey, n=200

Over half of publishers (55%) rated a Facebook property (Facebook, Instagram or WhatsApp) as ‘very’ or ‘extremely’ important compared with nine in ten (90%) for Google search and YouTube combined. Subscription businesses, especially those from Nordic countries, were more likely to rate Google higher as were CEOs and Managing Directors.

Google maxes out on importance because of its pervasiveness as both technology and audience provider, and their willingness to engage on some key topics that matter to our business. I can’t say that about any other platform.

UK subscription business

The differences in ratings are partly a reflection of the lower number of referrals that publishers now get from Facebook following algorithm changes. But there also appears to be a change in sentiment toward third party platforms in general. Many publishers have been burned by creating bespoke content only to find the goalposts changing or the monetisation slow to materialise.

Our platform approach is increasingly focused on bringing people back to us. We aren’t interested in building communities on external platforms for the benefit of that platform.

UK publisher, formerly with advertising model, now reader payment focus

Subscription-based publishers are increasingly looking at social media as a marketing and acquisition channel, not primarily as a place to engage users with content. Others are prioritising channels on the basis of monetisation potential, which may explain why YouTube also scores well in our survey. But detailed responses are also a reminder that there isn’t a one-size-fits-all approach. Magazine brands are still finding value with Instagram and Snapchat, while local news providers still see social media as critical for traffic referral and for engagement.

Even with the changes to the algorithm this year, Facebook continues to drive traffic to our sites with a speed and volume unmatched by other platforms. However we are seeing sharp rises in traffic from closed social networks such as WhatsApp.

Karyn Fleeting, Head of Audience Engagement, Reach PLC

What Might Happen in 2019

From feeds to stories and groups: The ephemeral story format has been around for a few years but Facebook says that stories will surpass feeds as the main way people share with friends within the next year.25 Stories are used daily by 150 million people on Facebook, 190 million on Snapchat, and 300 million on Instagram. WhatsApp status is also a story format, Netflix (movie previews) and YouTube have been experimenting with stories (originally called reels) and AMP stories debuted last year as an open web version that sits on top of some Google searches. These are now being surfaced in the Google News feed on Android devices – a distribution channel that will become more important this year.

Many publishers have been increasingly focusing on Instagram stories. The Guardian, which has 1.2m followers on Instagram, has developed a series of recurring story series including ‘Fake or For Real’, which explores a fake story before debunking it, and Brexit Bites – condensing and explaining latest developments in story format.

Story formats from the BBC, Washington Post and the Guardian

The ‘news feed’ is in many ways a hangover from the desktop era, whereas stories are made for mobile screens, demand more visual storytelling skills and rely heavily on the personality of the reporter.26 Publishers looking to attract younger audiences in particular will need to develop more of these skills in 2019.

Something gives at Snapchat: The youth-focused network is set to make a loss of around $1.5b in 2019 as it tries to rebuild its user base after a series of product mistakes.27 Snapchat has lost millions of users in 2018 to Instagram, which cloned many of its ideas for filters and mobile-friendly stories. Outside the US, Snapchat is finding growth difficult, which leaves the network looking for investment or even sale. Chinese internet giant Tencent already has a 12% stake. Disney or Amazon could also be interested.

Paid social networks: Suggestions that Facebook might offer an ad-free subscription version have been around for years, but it might just happen in 2019. Even if only a small number of people signed up, it could be a useful way to answer privacy concerns by offering an alternative that doesn’t involve harvesting personal data. The company already offers free and paid tiers for its enterprise social network Facebook at Work.

Platforms push further into video and TV: Online video is set to be a key battleground as platforms try to grab a share of the rapidly rising OTT (over-the-top) market. Apple has been building new entertainment studios in California and has been stockpiling shows for release in the spring or early summer. Bundling these with Apple Music could help with its subscription battle with Amazon Prime, Spotify and Netflix.

More relevant to news was the global launch of Facebook Watch in 2018, part of its strategy to move into longer form video. Along with IGTV (Instagram TV) these initiatives are part of a long-stated desire by Facebook to re-invent television in a more social and interactive way – and of course to take advertising dollars from incumbent players. These are also a direct assault on YouTube’s position as the home of user-generated online video and original content. Snapchat is also expanding its Shows feature to around 17 premium content partners in the UK28 and will be creating a space for Shows and Snapchat Originals within the Discover portal.

Facebook Watch and Snapchat Originals

Video does provide publishers with new opportunities to diversify, not least because competing platforms should make the value of original content higher. But as the experience of Mic.com shows, relying on platforms can be a high-risk strategy, after the company effectively folded when the money for Facebook Watch shows was pulled.

Duopoly becomes the triopoly: Amazon is becoming a growing force in the digital ad market. Research group eMarketer finds that consumers are increasingly starting product searches on Amazon rather than Google, enabling it to charge higher premiums. Overall Amazon has taken 4% of online ad spending in the US, a figure that is expected to rise to 7% by 2020.

Duopoly vs Amazon share of US digital ad spending 2018 and 2020

Source: eMarketer

The coming year will see platforms increasingly encroaching on each other’s once very separate territories. With mobile and internet growth slowing overall, the big four platforms (Google, Facebook, Apple and Amazon) will increasingly need to step on each other’s toes to keep moving forward.

2.1.3 Drumbeat around Regulation Grows29

In the last year the policy debate has shifted from whether to regulate the internet, to how. Germany got the ball rolling with the Network Enforcement Law coming into full effect at the start of 2018, but it was widely criticised for incentivising over-blocking by platforms, including content posted by politicians.

Since then we’ve had action or commitments to act by, amongst others, the UK, France, Germany, Italy, Australia, Singapore, Belarus, Kenya, and Sri Lanka. Even the US passed the FOSTA-SESTA legislation in 2018, which made platforms liable for sex-trafficking on their sites.30

The problem is that there is no real consensus on the different problems to be addressed, never mind on how these could be solved.

What Might Happen in 2019

Platform responsibilities for online harm redefined – but how? Platforms that rely on user-generated content and algorithmic recommendations have long resisted the notion that they are publishers. But they are now demonstrably facing up to their responsibility for the content they carry with the effort they are putting into identifying sexual grooming, bullying, terrorism, hate speech, undermining elections and other harmful behaviours. For their part, governments have also come to recognise that platforms are not utilities (like telecoms) nor are they publishers (like newspapers). So this year we will see an attempt to define platforms as a distinct category of their own. At Davos in January 2018 Teresa May said the ‘current situation was unsustainable,’31 and reiterated the need for a new definition for platforms with potential oversight in some areas. This idea is likely to be at the heart of a government white paper in the spring or early summer, assuming Brexit chaos doesn’t throw it off course. Elsewhere, an Australian inquiry (ACCC) has also recommended overhauling media regulation to include internet and platform companies.

Governments need to truly understand the complexity of the digital landscape and lack the expertise to do so. Platforms will only come to the table when they are really under threat. That moment has not come to pass just yet.

UK publisher

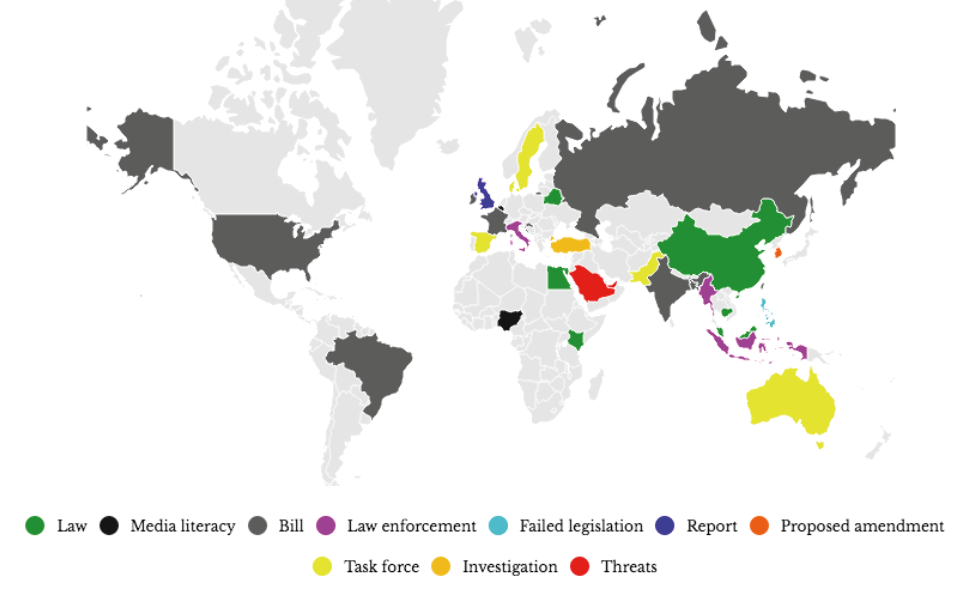

This year all eyes will be on Singapore, which is likely to pass one of the most draconian laws yet involving criminal penalties for those sharing ‘fake news’ or monetising falsehoods, which also impose rapid takedown requirements on platforms.32 Human rights and journalist groups are worried about who gets to define which news is ‘fake’ and the consequent implications for free speech. With Belarus33 and Kenya34 already attracting criticism for the arbitrary nature of their ‘fake news’ laws, the fear is that authoritarian leaders everywhere will be tempted to use public concern over misinformation to silence legitimate questions and increase government control over journalists and social media networks.

Where governments are taking action

Source: Poynter Institute, Daniel Funke (October 2018)

Source: Poynter Institute, Daniel Funke (October 2018)

Privacy a new platform battleground, US legislation likely: The Cambridge Analytica data leak contributed significantly to public concern about the safety of personal information with one poll conducted immediately afterwards showing that almost half (44%) had changed their Facebook privacy settings.35 Meanwhile Apple CEO Tim Cook has called for new digital privacy laws in the United States, warning that the collection of huge amounts of personal data by companies is harming society.

We have to admit when the free market’s not working, and it hasn’t worked here. It is inevitable that there will be some level of regulation.

Tim Cook, Apple CEO

Apple’s position can be seen as driven by self-interest given that it makes money by selling hardware and software, not from the personal details of its users. On the other hand, Facebook CEO Mark Zuckerberg has also recognised the need for some kind of regulation given that ‘the internet is growing in importance in people’s lives’36. He ‘s pledged to work with Congress as it develops protections for citizens over their own data, following the example of the European GDPR initiative. The Australian ACCC has recommended a similar approach.

Platforms, however, will want to proactively respond to head off regulation that could impact innovation or profits. Expect tech companies to offer more and clearer controls over data this year.

Copyright wrangles continue: Changes to EU copyright laws are complex, technical and have been going on for years, but some clauses are so controversial they have led Tim Berners Lee, the United Nations, a number of movie studios and four million ordinary Europeans to object. Article 11 states that publishers ‘may obtain fair and proportionate remuneration for the digital use of their press publications by information society service providers’. This means that any platform using more than ‘mere hyperlinks which are accompanied by individual words’ will require licensing. A similar piece of legislation in Spain led to Google News pulling out entirely leaving many smaller publishers worse off. Based on what happened when Germany passed a similar provision, some expect publishers to give major platforms the right to use snippets of content for free, but the details are unclear, as are the implications for large platforms, news aggregators and smaller start-ups and even news organisations that curate content from competitors.

Article 13 would essentially introduce automated checks of whether copyright had been infringed every time anyone publishes anything on the internet. Opponents say this is both impractical, expensive and dangerous – overprotecting dubious copyright claims and stunting creativity and innovation.37

If either of these clauses is implemented, it could have significant impact on the news industry and on ordinary people, but our bet is that there’ll still be no definitive outcome by this time next year.

2.2 The Business of Journalism

2.2.1 Publishers Focus on Subscription, but Limits Become Clear

It’s been another terrible year for many legacy media companies. Sharp declines in print revenue have hit the bottom line with digital unable to make up the difference. Although online advertising is still growing fast, very little of that finds its way to publishers because giant tech platforms like Google and Facebook can target audiences more efficiently and with greater scale and have the volume to offer lower rates. And these winner-takes-all dynamics in the advertising market have hit digital-born brands in the last year with venture capitalists looking to firesale their media investments. Against this background, we have seen a pivot to paid content or at the very least a push for more diversified revenue streams.

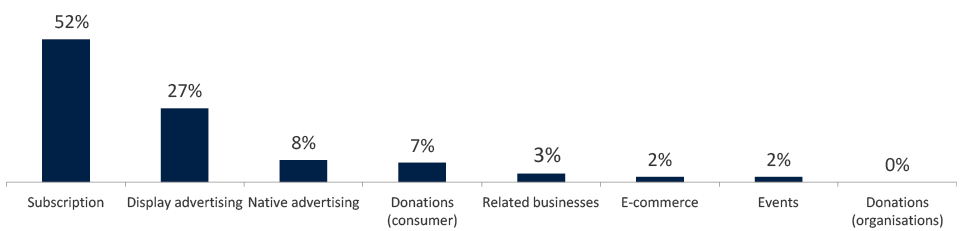

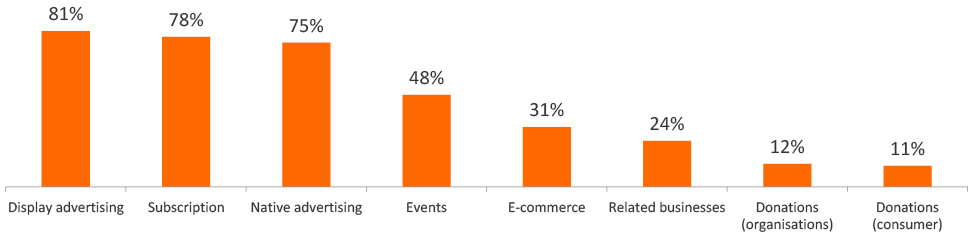

In our survey the extent of this pivot has become clear. For the majority of our publishers, subscription (52%) is now the main priority for the year ahead, followed by display advertising (27%), native advertising (8%), and donations/crowdsourcing from individuals (7%).

Main revenue focus in 2019

Q5. Which of the following digital revenue streams is MOST important for your company in 2019? Digital leaders survey 2019, N=163

Q5. Which of the following digital revenue streams is MOST important for your company in 2019? Digital leaders survey 2019, N=163

Important revenue focus in 2019

Q4. Which of the following digital revenue streams are important or very important for your company in 2019? Digital leaders survey 2019, N=163

Q4. Which of the following digital revenue streams are important or very important for your company in 2019? Digital leaders survey 2019, N=163

The differences between the two charts are illuminating. Display and native advertising remain important today but the key focus going forward is on building or strengthening businesses around subscription and donations.

Subscriptions is the key strategy, so the investment in driving subscriptions will be critical in 2019 and probably 2020 to create a sustainable news business.

Sergio Rodríguez, Digital Editor-in-Chief, La Razón, Spain

For many publications this will require different skills, new metrics, and an emphasis on higher quality content that is worth paying for. Some are learning about subscription for the first time, others have been building up their community for years:

We have more than 12,000 subscriptions, but growing subscriptions is not an easy task in a country where there is no culture of payment for digital content.

Laura Sanz, Product Director, El Espanol, Spain

El Espanol combines subscription with advertising and small-scale events that also produce content for the publication. The underlying story then is as much about diversification as a complete switch – with the average respondent to our survey saying that four different revenue streams are important to them. As digital strategist Adam Tinworth points out, ‘the best sites will combine membership with other revenue streams, like events, goods and even (whisper it) print’.

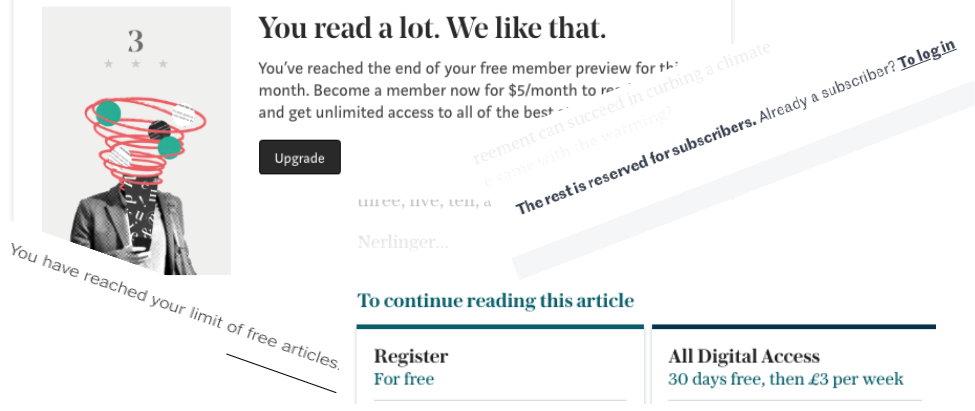

Limits of subscription could be hit in 2019

The coming year is likely to see ever-higher barriers to content as publishers push subscription strategies of various flavours. These range from putting whole sites behind a paywall, to the introduction of new tiered ‘membership’ models from the likes of the Independent and (possibly) HuffPost where certain content is kept back for loyal readers.

Quality news is disappearing behind paywalls

But these publisher-led strategies are likely to meet considerable consumer resistance in 2019. Our own research suggests that in most countries only a small minority is prepared to take out digital subscriptions – with the majority of casual users continuing to be happy with free advertising based services.38 One news subscription already looks expensive compared with Netflix (or Spotify), let alone two or three. In short, subscription barriers could end up annoying consumers further and giving people another reason to turn away from news.

Others are concerned about the wider implications for democracy if the rich end up with access to higher quality, more trusted information than those who can’t afford to pay. So what might give in the year ahead?

What Might Happen in 2019

Paywall blockers emerge: We’ll see growing adoption of ‘subscription blockers’, downloadable software or browser extensions that that get round metered paywalls by blocking the javascript that triggers them. Forcing users to login for any content is one way round this, but this will reduce fly-by users and the resulting advertising revenue.

Popular searches on Google

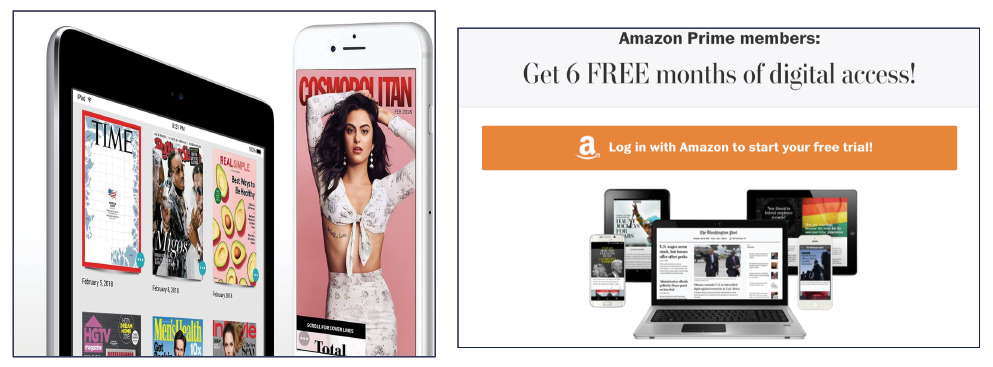

Bundling and payment aggregation: Companies are looking at increasing the value of their existing subscriptions as a way of reducing churn in the face of increased competition for readers who are prepared to pay. The Times of London has added a one-year Wall Street Journal subscription for existing subscribers while telecom and OTT video providers also experimented with adding news to their bundles. Amazon Prime membership in the US comes with a 6-month free trial of the Washington Post and reduced cost subscription to follow.

Meanwhile Apple has been wooing top publishers for a new subscription play,39 which may involve a recently acquired app called Texture – often described as a Netflix or Hulu for news – which currently lets consumers read as many stories as they want from dozens of magazines for $10 a month. This could be an appealing consumer proposition but successful paywall publishers will be extremely wary of cannibalising existing businesses. Publishers would prefer to integrate their own paywalls and price points within the Apple News app. Ultimately insiders say Apple may wish to bundle news, music and its new TV investments into a powerful alternative to Amazon Prime.

Apple gears up for more bundling; Amazon Prime deals with the Washington Post

2.2.2 Donation and Philanthropy set for a Boon

With subscription unlikely to work for all, interest in alternative models is growing. The Guardian’s strategy of keeping the internet open for all by appealing for donations from loyal readers has attracted much attention. Over a million people have given a one-off or continuing donation over the last three years and this could help the Guardian break even in 2019.

Donations work well for organisations with a clear political ideology, providing a substantial amount of income for partisan UK websites like the Canary and Novara Media. But giving money to a purely commercial organisation seems to be a harder sell. Buzzfeed’s recently launched membership scheme was widely ridiculed for trying to charge $100 a year for a tote bag and a few inside track emails.

Meanwhile project-based contributions from NGOs and philanthropists has become a major income stream for publishers with 12% of our respondents saying it will be important this year. Newsrooms across Europe have started to employ dedicated fundraisers and set up philanthropic business units.

There are more than 146,000 ‘public-benefit’ foundations in Europe with an estimated annual expenditure of €51 billion.40 These foundations rely on a stable environment which enables their programmes to be delivered and yet only a tiny fraction goes to core support for journalism, compared to US foundations.

In 2019, we will see a lot more foundations move into supporting journalism. This will not be as part of a PR or communication strategy, but as an investment into an infrastructure they all rely on. Similarly, more news organisations will realise that philanthropic investment can give breathing space to revenue model experimentation, or fund under-resourced areas of reporting (often science, health, or investigations).

Adam Thomas, Director, European Journalism Centre

Donation models could be supercharged this year by government initiatives to allow media companies to benefit from tax incentives when receiving charitable donations. The Canadian government made this a centrepiece of its proposals to make journalism more sustainable and the UK’s Cairncross commission is likely to recommend something similar early in 2019 with a special focus on helping local newspapers.

Direct subsidy back on the table in 2019

Some media companies are hoping governments will help them with tax breaks or other direct subsidy, as the Canadian government has just done to the tune of CAN$600m over five years. In addition to incentivising donations and subscriptions, commercial companies will be able to claim tax credits in return for publishing a ‘variety of news and information of interest to Canadians’.41 But others worry that relying on government money is ultimately a slippery slope that will undermine journalistic independence.

Subsidies from tech platforms – such as the $4.5m donation by Facebook for local journalism training in the UK – will also increasingly be on offer this year, but these tend to be time-limited and come with strings attached.

Governments haven’t got any money, the industry shouldn’t be a charity case, and platforms only spend when it’s an investment. I’m not hopeful. The industry should do more to save itself.

UK publisher

Commercial companies will increasingly have to deal with these dilemmas as it become clearer that parts of their traditional business are subject to market failure. How to combine commercial and public models will be an increasingly important part of the next phase of the digital news journey.

Where can the media expect most help in 2019?

Q10. Who do you think are most likely to provide significant additional support for journalism in 2019? Digital leaders survey, N=192

Government subsidies are growing in China and Russia

The weakness of western media may not just be a problem for the companies themselves. It is striking that many authoritarian countries are investing directly in media (and propaganda) like never before. China, for example, is opening a new state of the art European TV hub in west London at the start of 2019 and will be pumping out news with a Chinese perspective in multiple languages – even as western news agencies and media companies are forced to scale back their foreign reporting:

The Governments in countries which are currently not [at] the forefront of liberalism show great interest in providing money for media. State-funded (and -controlled) players like Chinese Xinhua or Turkish Anadolu Agency are opening up offices all over the world, providing national media companies with ‘free’ (state-funded) news services.

Bernhard Sonntag, APA, Austria

2.2.3 Broken News: Could Slow News Help?

Digital and social media has incentivised poor quality, repetitive and shallow journalism – so say the critics. But how might this change if readers set the agenda rather than advertisers? Could less journalism be better for society and create more impact?

These are some of the questions that have inspired the ‘slow news’ movement which we’ll be hearing much more about in 2019. Tortoise Media is the brainchild of former BBC Director of News, James Harding, along with co-founder Katie Vannick-Smith, most recently President at the Wall Street Journal. The project, which launches in April 2019, promises to create a ‘different kind of newsroom’, involving daily open news conferences called ‘Thinkins’. It will largely ignore breaking news but tackle four or five stories each day through its website, app and newsletter. Money has come from a range of backers but also from a Kickstarter crowdfunding campaign, which raised around £500,000 from 2,5o0 initial members, many of whom are under 30.

Tortoise Media Thinkin, December 2018

Source: author photo

Source: author photo

Attending one of first ‘Thinkins’, which looked at the ethical dilemmas of AI, it was fascinating to see how ideas were drawn from Tortoise members who had direct experience of using AI in banking, and the police. Co-founder James Harding wants these conferences to ‘work as events but also as an engine for our journalism’.

Tortoise is targeting 40,000 paying subscribers by the end of the year, but will supplement this with sponsorship and regular live events.

One inspiration for ‘slow, thoughtful’ news came from the Dutch start-up De Correspondent, which is now taking the idea to the United States and is due to launch in mid-2019. Over 45,000 people have invested in this ‘movement for un-breaking news’, contributing over $2.5m via Kickstarter. De Correspondent is billed as an antidote to the endless scroll of digital platforms and the stream of news notifications. Like Tortoise, it taps into a desire to slow down, to consume deeper and more meaningful journalism, but also to connect with like-minded people.

One inspiration for ‘slow, thoughtful’ news came from the Dutch start-up De Correspondent, which is now taking the idea to the United States and is due to launch in mid-2019. Over 45,000 people have invested in this ‘movement for un-breaking news’, contributing over $2.5m via Kickstarter. De Correspondent is billed as an antidote to the endless scroll of digital platforms and the stream of news notifications. Like Tortoise, it taps into a desire to slow down, to consume deeper and more meaningful journalism, but also to connect with like-minded people.

Until now, the slow news movement has been limited in terms of its impact and scale – but there is no doubting the ambition of these two projects. It will be fascinating to see if these bold experiments in journalism can reach beyond a small number of concerned citizens and ultimately make enough money to survive.

2.2.4 Collaboration on the Rise

News organisations have traditionally been highly competitive at every level but could that change in 2019? More co-operation could help create the scale to counter platform power and defray the costs of ever more complex technology. International journalistic collaborations have also demonstrably created impact around subjects such as the Panama Papers, while Bureau Local in the UK has shown the value of combining centralised data collection and analysis with strong local reporting. Fact-checking initiatives such as Comprova in Brazil and Verificado in Mexico have forced newsrooms to work together in new ways at election time.

Our survey shows strong support for these trends with over two thirds seeing the value of common technology (71%) and advertising (67%) solutions. The idea of sharing journalistic resources or content was more contentious with only half in favour (50%).

Should news organisations co-operate more?

Q10. News organisations have traditionally been competitive, but should that change? To what extent do you agree that they should …? Digital leaders survey, N=192

Broadly I think publishers should look to a model where we share technology which solves our common issues and then use our journalism to differentiate our output.

UK publisher

Joint initiatives

The Washington Post has been making the running on technology with its ARC Publishing Platform, which it has built from scratch to build pages, manage paywalls, test headlines, distribute content post to outside platforms, as well as collecting and analysing data. So far more than a dozen publishers have bought at least part of the system including the Canada’s Globe and Mail, El País in Spain and Infobae in Brazil. The Post thinks this could be worth $100 million a year in revenue within a few years with a profit margin of over 60%.42 Vox Media is also trying to licence use of its highly regarded Chorus publishing suite, which powers its own titles, The Verge, Vox and Recode. But lining up customers willing to pay six- and seven-figure sums for publishing technology may be a tall order in a digital media industry where money is in short supply.

Meanwhile a range of other publisher initiatives is likely to progress further in 2019. News UK, Telegraph Media Group, the Guardian, and Reach/Trinity Mirror plan to develop Ozone, which is building a technology stack for advertising. The Ozone Project is a standalone (non-profit) business that is trying to solve issues that affect everyone – saving time and money for all. As one example, it is developing a common taxonomy for content that allows advertising to be sold in a consistent way across titles.43 It is also lobbying for common advertising identifiers, which could make programmatic processes quicker and simpler, reducing page load times. Expect more publishers to sign up in 2019.

Publisher initiatives are also progressing around trying to forge a common login. In Germany 20 publishers, e-commerce operators and ISPs have got together to create a trusted alternative to Facebook or Google login systems. The Net ID alliance hopes to provide a single location for consumers to manage their preferences around privacy and advertising consent. Publishers know that a more personalised future depends on direct relationships while the prospect of a new EU e-Privacy Regulation,44 which could make it harder to use cookies to identify users, is also spurring publishers in France45 and Portugal46 to find better ways to identify users with appropriate consent.

2.2.5 Diversity and Retaining Talent an the Newsroom

The explosion of content and the intensity of the 24-hour news cycle have put huge pressure on individual journalists over the last few years. This at a time when the relative status and pay of journalists has declined compared with other professions.

Our survey shows that newsroom leaders are concerned about diversity (56%), burnout (62%), and the ability to attract (73%) and retain talent (74%).

Concern about talent and burnout in the newsroom

Q9. Rate your level of concern about the following issues (showing code for ‘concerned’ and ‘very concerned’). Digital leaders survey, N=193

Q9. Rate your level of concern about the following issues (showing code for ‘concerned’ and ‘very concerned’). Digital leaders survey, N=193

Looking at the detailed results, burnout concerns were most keenly felt in editorial roles whereas talent attraction and retention issues applied particularly to product and technical roles.

For Journalists, we’re still a good address. For technical and IT staff, we struggle to meet market levels (pay, conditions, career opportunities).

Swiss publisher

Leading a group of product, UX and tech, News and Media is a long way from first choice for most talented staff.

Product Head, leading UK publisher

Some publishers report a growing tension between the pay levels of technical staff and those of journalists. Meanwhile radio broadcasters report difficulties in retaining editorial talent with the boom in podcasts opening up new opportunities for presenters and producers.

Diversity in the Newsroom

The issue of gender equality has been a focus in the last year in the UK where media companies were forced to reveal pay gaps between men and women for the first time. Press Gazette analysis showed that 91 per cent of UK-based media companies paid men more than women and that men occupied the vast majority of senior roles. More widely, the Global Media Monitoring Project has shown than women are ‘dramatically under-represented in the news’ with less than a quarter (24%) of news subjects or interviewees being female.47 In the UK, footballer Raheem Sterling and singer Jamelia have spoken out about the negative way in which black people are reflected in the media – again highlighting the need for greater newsroom diversity. And in the US, there is an increasing focus on political diversity with many newsrooms accused of anti-Trump bias and being out of touch with middle America.

The vast majority of our industry is populated with liberals. The world is not as overwhelmingly liberal as the news industry, making us a bit out of step with a good number of potential paying readers. What are we going to do about that?

David Grant, Associate Publisher, Christian Science Monitor, USA

With times increasingly tough, publishers can’t afford to alienate any audience. In 2019 expect to more awareness of the link between diversity and business success.

What Might Happen in 2019

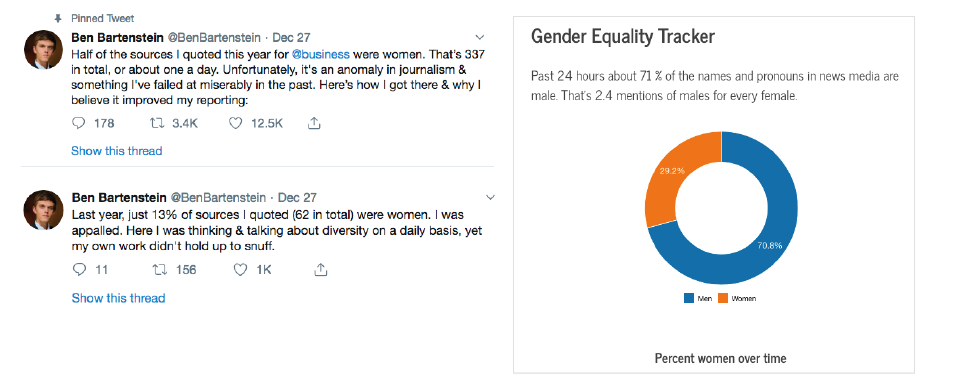

Changing journalistic practice: Expect more journalists to follow the example of Bloomberg business reporter Ben Bartenstein who found that only 13% of his interviewees were female and set out to remedy that – achieving his 50% target by proactively seeking out new and more diverse sources. Colleagues helped build up lists of high profile women in finance while Bloomberg launched a New Voices initiative to give media training to women executives. In a Twitter thread, Bartenstein argues48 that this has given him a competitive advantage and leads to more interesting and higher impact stories.

Gender awareness thread; gender equality tracker (United States)

Diversity metrics: More newsrooms will start to use automated tools like Prognosis (see figure above) that monitor gender and ethnic diversity of content on websites by counting the names of interviewees49 or analysing pictures.

This awareness in turn will make editors more aware of their own biases. The Financial Times has created a dashboard that monitors the reading habits of existing female subscribers to encourage editors to create more content that might appeal to women. But deeper research on gender preferences has also led to new products such as the Long Story Short newsletter, five stories you shouldn’t miss, curated by a female FT journalist. One unexpected by-product was that this newsletter also proved a hit with disengaged male readers.

2.3 AI and the Newsroom

Publishers tell us that they are planning to invest more this year in harnessing the potential of Artificial Intelligence (AI) and Machine Learning (ML) – but not at the expense of editors and journalists. Our survey shows respondents think that investment in AI (78%) and more journalists (85%) is needed to help meet future challenges – but with strongest preferences heavily stacked in favour of humans.

Editors still matter more than machines, say editors

Q6. To what degree do you agree with the following statements? Digital Leaders Survey 2019, N=195

Q6. To what degree do you agree with the following statements? Digital Leaders Survey 2019, N=195

We need a mix of both AI and human intelligence.

Ritu Kapur, CEO The Quint, India

We always need more journalists. However we must also invest in technology to help those journalists be as efficient as possible so they can pursue the work with the highest impact. In addition, AI investments will help us serve our audiences and combat misinformation.

We always need more journalists. However we must also invest in technology to help those journalists be as efficient as possible so they can pursue the work with the highest impact. In addition, AI investments will help us serve our audiences and combat misinformation.Lisa Gibbs, Director of News Partnerships, AP

Last year 72% of publishers said they were experimenting with AI, but this year we can expect to see more real life deployment. This will fall into three main categories:

1) Using ML to personalise content and create better recommendations for audiences;

2) Automating more stories and videos (so called robo-journalism);

3) Providing tools to help augment and support journalists deal with information overload.

2.3.1 Personalisation and Recommendation

Chinese news apps like Jinri Toutiao (Today’s Headlines), Qutoutiao and Kuaibao are currently leading the world in their use of AI (mainly machine learning techniques) to deliver personalised news from a range of news providers. Toutiao has around 120m users with average dwell times of over an hour each day. Now these AI driven apps are spreading across Asia with Newsdog one of the most popular aggregators in India and Toutiao’s owners, Bytedance, investing in similar apps in Indonesia.

Toutiao and Newsdog

Engagement may be high, but the dangers of this approach are also becoming apparent. Popularity based algorithms are encouraging clickbait, a surfeit of viral videos and other sensationalist material. The Chinese government suspended a number of apps including Toutiao in April 2018 for carrying vulgar and untrue material.50 Just like social media platforms, aggregator apps will need to start facing up to their wider responsibilities this year and that will increasingly mean putting in some kind of editorial oversight.

Personalisation of the news service is critical, but does not mean just handing over editorial judgement to algorithms …

UK publisher

The big question for traditional publishers is how to use AI responsibly and transparently within their own websites and apps and how to communicate what is going on to users. The Finnish broadcaster YLE has spent a lot of time thinking about these issues as it develops its Voitto intelligent assistant (left). This collects feedback on AI-driven recommendations directly on the lockscreen – the first app to do so – and aims to build an on-going dialogue with users about the choices they make. Critically it does not use click through rate (CTR) as the main measure of success but rather how many people keep the Voitto assistant on and whether they are happy with the number and type of recommendations they receive (76% say they are).

The big question for traditional publishers is how to use AI responsibly and transparently within their own websites and apps and how to communicate what is going on to users. The Finnish broadcaster YLE has spent a lot of time thinking about these issues as it develops its Voitto intelligent assistant (left). This collects feedback on AI-driven recommendations directly on the lockscreen – the first app to do so – and aims to build an on-going dialogue with users about the choices they make. Critically it does not use click through rate (CTR) as the main measure of success but rather how many people keep the Voitto assistant on and whether they are happy with the number and type of recommendations they receive (76% say they are).

In 2019 the BBC will also be thinking more about what a ‘public service algorithm’ could be. This will mean educating listeners about the benefits of algorithms and how to use personalisation options without unintended consequences (such as removing views that may challenge your own).

Charlie Beckett, who runs the Polis project at the LSE, will also be exploring these issues for a new Google-supported project focused on research and AI training for newsrooms. He sees the pitfalls ahead: ‘There are a host of editorial/ethical issues around the transparency (or lack of it) and the biases of these algorithms and programmes. The last thing journalism needs now is to further dilute trust and transparency in its work.’

2.3.2 Robo-Journalism

News agencies have been automating news stories around company earnings for years, but the next step seems to be virtual newsreaders. China’s state news agency, Xinhua, has unveiled a robotic news anchor that is ‘ego-free and always ready for work’. Computer programmes have modelled the voices, lip movements and expressions of real Xinhau presenters to create these simulations. These early versions tend to show a lack of warmth, but experts believe that eventually even a sense of humour could be programmed in. In a similar vein, Japan’s national public broadcaster NHK has created anime newsreaders that can sign news for those with hearing impairment, or co-anchor the main evening news bulletin.

Which news anchor is real? Could Anime reporters replace humans?

Source: Xinhua, NHK

The latest NHK experiment, Yomiko, was designed by a leading manga artist and has the personality of a fresh-faced cub reporter. She has featured within the main news bulletin (above) but also has a presence of her own reading the news via Amazon Alexa and Google Home.

These technologies have significant potential to make existing processes quicker and more efficient, but also to create output that was previously not viable. YLE’s previously mentioned Voitto assistant is now generating around 100 sports stories and 250 illustrations each week. News agencies are ramping up their production too with the Finnish news agency STT translating news into English and Swedish automatically. By the end of this year, AP aims to have produced 40,000 automated stories, primarily in business news and sports. Next steps will be to make the labelling and captioning process easier using image recognition software for the newsroom.

2.3.3 Tools to Support and Augment Journalists

The speed and amount of news now make it increasingly necessary for journalists to use algorithms to help find stories and verify them in real time. DataMinr used AI to sift through millions of tweets. Its algorithms help spot unusual patterns that help newsrooms to keep on top of breaking news. AP has developed an internal verification tool, which helps journalists verify multimedia content in real time.

The Reuters news agency is taking a different approach, building an AI tool to help journalists analyse big data sets and suggest story ideas. It may also help write part of the story, though the aim is not to replace reporters. In the year ahead, it is likely that these tools might increasingly scoop journalists as patterns in data provide new areas to explore.

And how can journalists prepare for the AI future?

A Finnish university is offering a free course, open to anyone in the world, as part of a drive to increase public understanding. It takes around 30 hours to complete and international students will get a certificate that they can post to their LinkedIn profile.51 Amazon has also opened up an internal course designed for its developers to all-comers. Expect more public and private initiatives in 2019.

2.4 Audio and Voice in 2019

Audio looks set to be one of the hottest topics in media during 2019, driven by the growing popularity of podcasts and the sale of hundreds of millions of new audio devices (aka smart speakers) – now spreading rapidly across the world. It is estimated that up to 40million people own smart speakers in the United States and about 7million in the UK.52

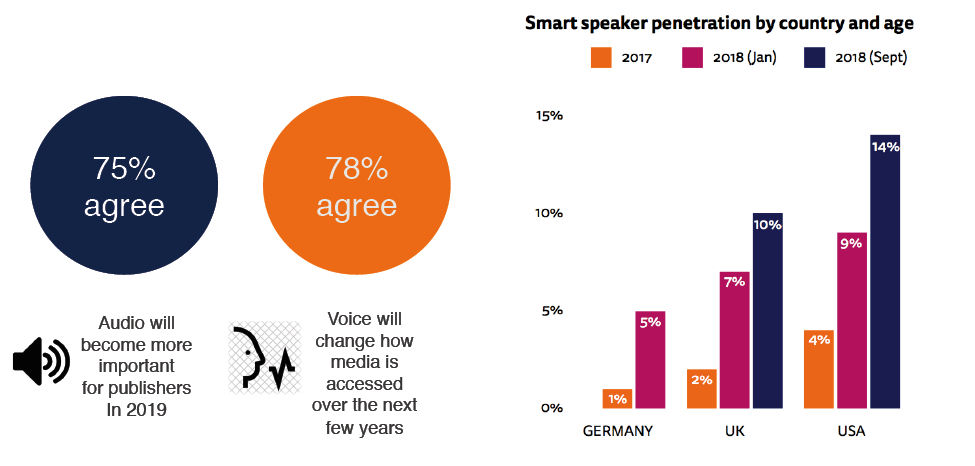

In our digital leaders survey, three quarters of respondents (75%) say that audio is becoming a more important part of content and commercial strategies with many publishers now building up bespoke audio production units. The vast majority (78%) also think that voice-activated technologies (Amazon Alexa, Google Assistant) will transform the way audiences discover media over the next few years.

Publishers think audio represents a big opportunity in 2019

2017/Jan 2018 Digital News Report Q. Which, if any, of the following devices do you ever use (for any purpose)? Showing smart speaker code. Base: All (approx. 2000 in each country). RISJ Smart speaker survey (Sept 2018) Q. Which of the following devices do you own and use nowadays? Showing smart speaker code. Base: All, UK=2104, US=3288.

2017/Jan 2018 Digital News Report Q. Which, if any, of the following devices do you ever use (for any purpose)? Showing smart speaker code. Base: All (approx. 2000 in each country). RISJ Smart speaker survey (Sept 2018) Q. Which of the following devices do you own and use nowadays? Showing smart speaker code. Base: All, UK=2104, US=3288.

Podcasts got newsier over the last year as more publishers looked to follow the success of The Daily from the New York Times, a broadcast which has over 5m listeners a month and has now extended its footprint to linear (public) radio. The Guardian (Today in Focus), and the Washington Post (Post Reports) are two other publishers that are investing heavily in audio, partly because they see a good business opportunity and partly as a way of reaching younger audiences. Our own research shows that under-35s are between three and five times more likely to consume podcasts compared with traditional speech radio.

Voice-activated technology/audio will be one of several platforms, suited for certain types of news consumption (morning briefing for example). The danger is a ‘pivot to video’ one of publishers thinking it will become THE dominant platform/journey.

UK publisher

Scepticism about the sustainability of the buzz around podcasts was fuelled by Buzzfeed’s decision to cut its in-house podcast team in 2018, as well as editorial lay offs at Audible Originals and Panoply. Damian Radcliffe from the University of Oregon thinks we may already have hit peak podcast: ‘There are simply too many to listen to’ he says. ‘As a result, many new efforts, including a lot of really good ones, may fail to find an audience – or the size of audience – that they need to survive.’ But optimists point to strong user demand and significant increased promotion and interest by major platforms.

- Google’s podcast app launched in June and is accompanied by a creator programme to encourage more diverse content, including a push to generate more voices from non-developed nations.

- Spotify opened up its platform up to all producers in October and is signing up more original shows including a bilingual podcast about a drug cartel leader from Vice News.53

- Pandora has rolled out the podcast genome project to help discovery and recommendation.

With music streaming becoming more competitive, leading players could be looking at exclusive podcasts as a way of driving growth and reducing churn. Podcasts may not offer a pot of gold, but easier access, better discovery and millions of new audio devices suggests there is considerable growth left in the market.

Voice activated speakers and assistants

Though millions of smart speakers were unwrapped at Christmas, the story of the coming year is likely to be the spread of voice assistants outside the home and to many more languages.

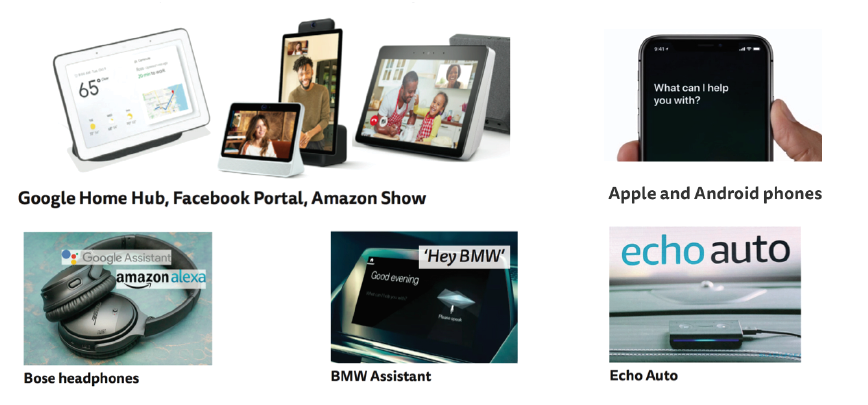

New iOS and Android operating systems have made voice more prominent on mobile phones, headphone manufacturers like Bose are embracing them while car manufacturers are launching their own assistants as well as making it easier to access Alexa, Google Assistant and Siri. All this will make it easier to access existing linear radio, podcasts, audio books and streaming music services in more places and in more convenient ways.

Not just smart speakers

But as our recent report on voice suggests,54 we’ll also see the development this year of more bespoke audio services like voice search, voice-activated games, and step-by-step audio recipes. But while voice makes accessing existing media more efficient, it’s not so good at expressing complex outputs or allowing navigation within audio experiences. This is why smart speakers are increasingly coming with screens that can display accompanying images such as weather maps as well as enabling video calling and picture display. The Google Hub (October 2018) is a screen-based smart speaker that adds a visual layer to voice-driven experiences, competing with the existing Amazon Show. Facebook also entered the market in October with Portal, a new screen-based device, which contains Alexa voice functionality as well as its proprietary voice recognition for video calling.

More languages in 2019?

|

Amazon Echo etc |

Google Home/Mini etc |

Apple HomePod |

|

|

2014 |

US pre launch (Nov 2014) US public launch (June 2015) |

||

|

2016 |

UK & Ireland, Germany (Sept) |

US launch (Nov) |

|

|

2017 |

India, Canada, Japan (Nov) |

UK (Apr), Canada (June), Australia (July), France (Aug), Germany (Aug), Japan (Oct) |

|

|

2018 |

Australia, New Zealand (Feb), France (June), Italy, Spain (Oct)

|

Italy (Mar), India, Singapore (Apr), Spain, Mexico, Ireland, Austria (June), South Korea (Sept), Sweden, Norway, Denmark, Netherlands (Oct) |

US, UK, Australia (Feb), Canada, France, Germany (May), Spain, Mexico (Oct)

|

The number of supported languages doubled in 2018 and we can expect the number of supported languages to grow further this year as the platform wars intensify. Samsung will join the party with its own range of speakers and screens powered by Bixby while Chinese, Korean and Russian tech giants have also developed their own range of branded devices with underlying AI assistants.

Opportunities for publishers

While publishers recognise that voice will be a major disruption, they are not clear about whether now is the right time to invest. Our own study suggested that the take up of news content was disappointing. Just 22% used news briefings daily in the UK and 18% in the US. Only 1% said that news was the most important feature, compared with 64% who cited playing music and 7% checking the weather. Much of the early usage has gone to default broadcasters like the BBC in the UK, ABC in Australia, and ARD in Germany, leaving little traffic for others. In general broadcasters are bullish and newspapers more cautious.

I think voice has the potential to fundamentally change the way people interact with our journalism.

Australian broadcaster

There are two major unknowns at this point – the extent to which consumers are actually into this thing, and whether or not it’s a genuine commercial opportunity.

UK newspaper publisher

Likely developments in voice this year

Publishers, who already fear their brands will be devalued in a voice environment, will be worried about this development. Publishers like the BBC prefer to create their own destinations (these are called skills or actions in a voice world) where they can offer more personalised and controllable audio – as well as offering onward journeys to other content.