Executive Summary

This year’s key developments will centre on online video, mobile apps and further moves towards distributed content. Mounting problems around online display advertising will lead to a burst of innovation around journalism business models.

More specifically…

- Facebook/Google/Apple battle intensifies over the future of mobile and the discovery of content

- Messaging apps continue to drive the next phase of the social revolution

- Mobile browsing speeds up thanks to initiatives by platforms and publishers

- Ad-blocker/publisher wars move to mobile – they rage through 2016

- Fraud and fake traffic further undermine faith in online advertising

- Renewed focus on paid content of different flavours (given above) including crowd funding, membership and micropayment

- Explosion of 360° video, auto-play video and vertical video (get used to it!)

- Growth of identified web (sign in and registration will be critical to delivering cross platform personal content and notifications)

- Breakthrough year for Robo-journalism– strikes in newsrooms over job losses

- Another year of spectacular cyber attacks and privacy breaches

- More measurement of attention/impact, less measurement of clicks

- Messaging apps go mainstream at work (eg Slack, Hipchat, FB at work)

- Scheduled TV viewing on the slide as more viewing shifts to on demand

- Rebirth of audio driven by internet delivery to mobile devices

Technology to watch for

- Virtual Reality (VR) hype goes into overdrive; but leaves non-gamers cold

- Artificial intelligence (AI) and messaging bots

- Bendy and flexible phones; wireless charging finally takes off

- Drones go mainstream with registration required in most countries

- Smart mirrors just one example of growing visibility of the Internet of Things

Everywhere we will see the growth of analytics and data informed decision-making in technology, marketing and even publishing. In a few years’ time, it will seem extraordinary how uninformed we once were

In our survey of 130 leading Editors, CEOs and Digital Leaders for this report…

- 76% said it was extremely important to improve the use of data in newsrooms

- 79% said they would be investing more in online news video this year

- 54% said deepening online engagement was a top priority

- 22% were more worried about online revenues than last year; though surprisingly 20% were less worried

(More data and comments from this survey throughout the report)

Companies, apps or technologies you’ll have heard of this time next year

include Symphony, Brigade, Newsflare, TheQuint, Forevery, Leap Motion, HTC Vive and the UC browser

It will be another big year for mergers and acquisitions (M&A)

We could see any of the following …

- Axel Springer buys more media companies

- News Corp buys more tech companies

- BT (or foreign company) buys ITV

- Apple buys Box (or Dropbox)

- Twitter buys Nuzzel

- Twitter is sold

- Yahoo is downsized/sold/broken up

- A brand buys a publisher

1. Looking Back to 2015: A Year of Distributed Content, Autoplay Videos and Animated Gifs

The defining development of the year was the emergence of new hosted and aggregated distribution models for news. These initiatives by a number of big tech companies (see below) will impact publishers for many years to come.

Snapchat Discover (1) led the charge in January by inviting publishers to create ‘native’ and mobile experiences on their platform. Facebook followed with Instant Articles (2) designed to create a faster and slicker experience– and promised publishers greater reach along with up to 100% of advertising revenues. The re-launched Apple News (3) also required media companies to publish content directly into their platform while Twitter Moments (4) is also about creating native experiences but interestingly involves reverse publishing that content within news sites to attract more people to Twitter.

By contrast, Google’s hosted content play, Accelerated Mobile Pages (AMP) was launched as a beta in October and is more of a technical standard that allows publishers to speed up their mobile web pages. It is in Google’s interest to keep webpages open and accessible to search services where it makes most of its money.

For publishers, these moves raise huge dilemmas. If more consumption moves to platforms like Facebook, Google, Twitter and Snapchat it will be harder to build direct relationships with users and monetise content. But if they do nothing, it will be hard to engage mainstream audiences who are spending more time with these platforms.

Quotes from the survey: our key challenge will be …

“Whether or not the titanic battle for open vs. closed web plays to the advantage of publishers or fast-tracks their demise”

“More distribution and consumption over third party channels – Google AMP, Instant Articles, Apple News – over which we have little control”

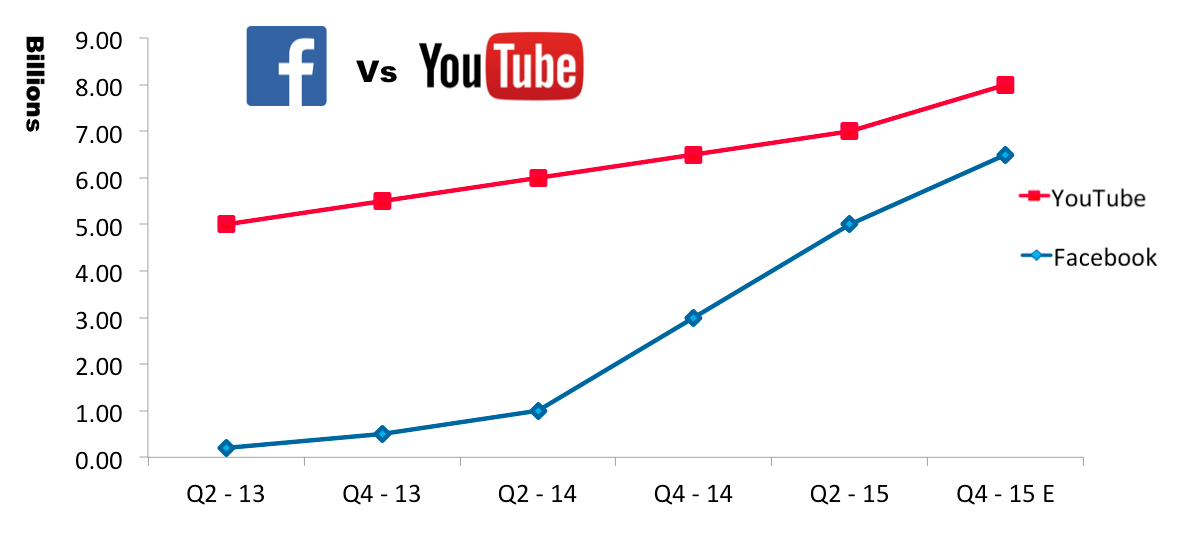

Further driving the move to distributed content was the explosion of native video in 2015. Facebook’s autoplay functionality helped it deliver 8bn videos a day globally (around 4bn in the US) by November – that’s a 100% increase in seven months with 75% delivered through mobile.1

US daily video views (NB. Facebook counts views @ 3s, YouTube @ 30 s)

Source: Company data and Activate analysis.

Twitter also opened its video platform to publishers, adding autoplay in 2015, while Google announced plans to white label its video player for free to publishers, a move that will drive far more professional news content through the YouTube network.

Monetisation of video remains an issue for 2016 with all eyes on Facebook.

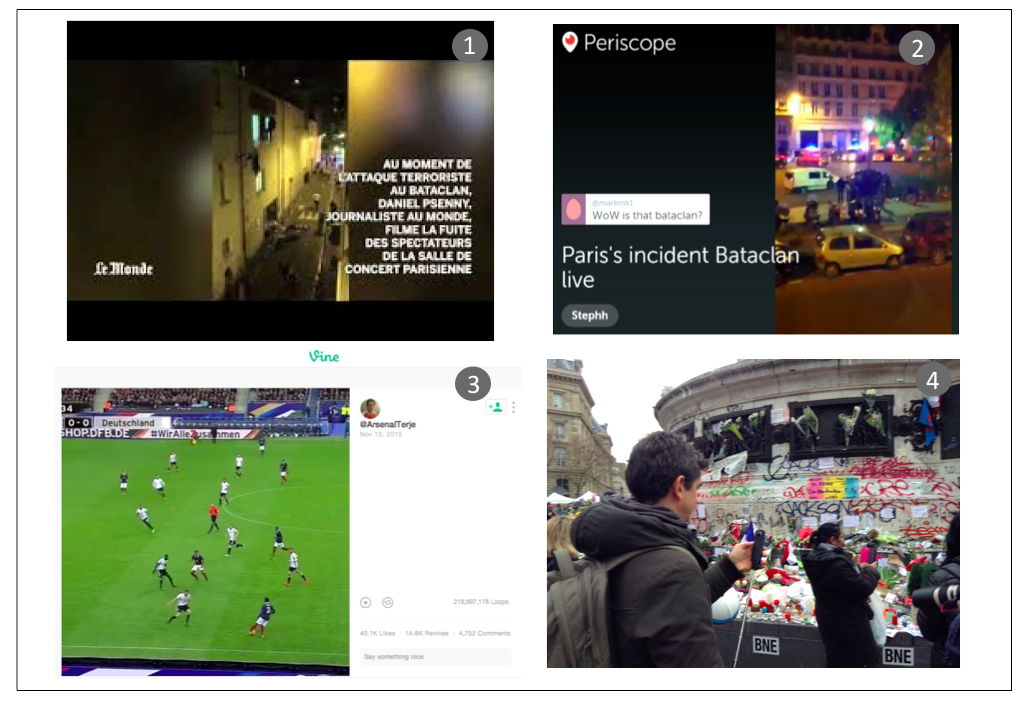

Video, social and visual content also defined coverage of the most dramatic news stories of the year including the Paris attacks.

In some of the most widely seen video footage, Le Monde journalist Daniel Psenny captured the graphic scenes as crowds fled the Bataclan concert hall in Paris on his iPhone (1).

In some of the most widely seen video footage, Le Monde journalist Daniel Psenny captured the graphic scenes as crowds fled the Bataclan concert hall in Paris on his iPhone (1).

Twitter user Stephane Hannache was one of many using live streaming app Periscope 2 hosting more than 10,000 viewers (2). A Vine video from the Stade de France – with clearly audible explosions – was one of the first verified accounts of the attacks (3). BBC correspondent Matthew Price filmed an immersive 360 video at the Place de la République (4) using a cheap simple consumer mobile device 3.

It is interesting to note that much of this video is square or vertical. It was created on mobile phones and was largely consumed on them too.

From Paris to Syria and beyond, 2015 saw the video enabled internet rivalling television news as the most compelling and authentic destination for live news. That’s a trend, which will increasingly put pressure on 24-hour broadcast channels in particular.

More than ever before, social platforms also played a key role in co-ordinating help and spreading information. Parisians used the Twitter hashtag #PorteOuverte (open door) to offer shelter in their homes, while Facebook deployed its Safety Check feature encouraging people in Paris to check in via their personal account – for the first time outside a natural disaster.

New Media Giants Consolidate as VC Money Moves On

As predicted last year, the global news media companies of the 21st century are beginning to emerge with significant further investment. NBC Universal put $200m into Buzzfeed, valuing it at $1.5bn – about twice as much as the year before. 4

Disney became the latest to invest in Vice, now valued at at more than $4bn5. Strategist Kevin Anderson says these two players are the major winners in this first round of new media monopoly:

“Buzzfeed and Vice have won this heat. We’ll see other players like Vox and Mic battle for third place, but …VCs are already cashing out and moving on from media investments to the next big thing”

It may be that 2015 will mark the high water mark in terms of valuations of digital news companies. Indeed the bubble has already burst for some with the closure of Circa in June, a shock given its reputation as a poster child for mobile-first media. Circa inspired fresh approaches to news delivery but ultimately never worked out how to make money itself. 6 Pioneering tech blog Gigaom was another high profile casualty of the brutal economic realities of news economics – having blown $20m of venture capital money.

Elsewhere, we saw a number of high profile acquisitions in the digital space. Flipboard bought mobile news aggregator Zite and then shut it down. 7 Germany’s Axel Springer bought Business Insider for $343m as part of its strategy to drive growth in the English-speaking world. (It also holds stakes in Politico Europe, Blendle, Mic.com and Ozy)8.

Nikkei bought the Financial Times for similar reasons in a $1.3bn deal while News Corp has been aggressively investing in digital start-ups like social video ad platform Unruly Media. Consolidation in local media saw the UK’s Trinity Mirror buy Local World in a bid for scale while many metro papers in the US are under pressure from local TV news flush with election cash and mobile apps providing local entertainment information.

But the news business is as much about people as technology. 2015 was a digital merry-go-round with digital born players and tech companies snapping up old media talent – and just a few going the other way. Janine Gibson moved from the Guardian to Buzzfeed along with other key staff, Cory Haik went from the Washington Post to Mic.com and Kate Day from the DailyTelegraph to Politico Europe. Liz Heron moved from Facebook to the Huffington Post.

Finally, as we pull together the strands of the year, we’re grateful to Paul Bradshaw at Birmingham City University for reminding us that many of the other big trends of 2015 had a distinctly retro feel:

- GIFs have re-emerged as a mainstream form of visual communication.

- Emojis – effectively emoticons on steroids – have done the same.

- Email newsletters have been re-invented; key distribution channels once again.

- So are podcasts – again (NPR reports downloads up 41% year on year).

- Chat apps are the new social media. Remember AOL and MSN Messenger?

- And platforms are becoming publishers – again. Just like Compuserve & AOL.

Last Year’s Predictions

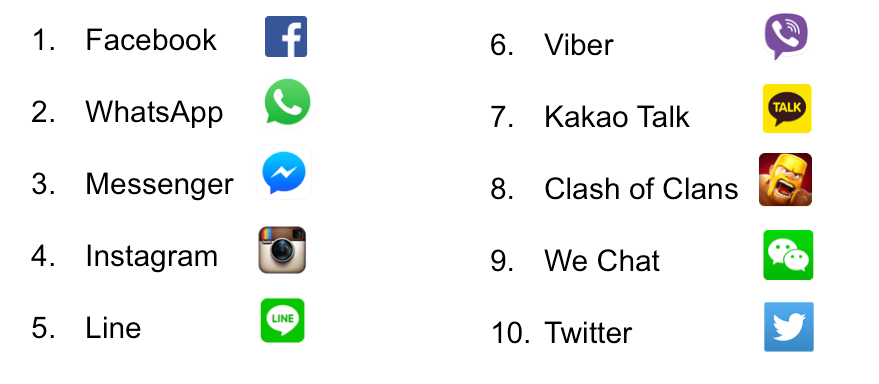

This time last year we said Ad-blocking would go mainstream (now around 20% in the UK and 40% with the young according to YouGov) and that more of us would spend more time with messaging applications. Nine of the top ten apps are now social or chat apps.

Top apps by usage (global – from Mary Meeker annual trends slide 47)

We predicted more high profile privacy leaks and cyber attacks. The most prominent at extramarital affair website Ashley Madison compromised intimate data for more than 30 million accounts.

Even the BBC website was brought down for several hours – allegedly by an anti-IS hacking group who’d been honing their techniques.

We suggested the Apple watch would sell around 20m in its first year, which looks like an over-estimate but it was another year of impressive product launches including the iPhone 6s, iPad Pro, Apple Pay, Apple Music & Beats 1.

Babies and the Next Billion

Last year we talked about the importance of internet.org the Facebook led initiative to bring cheap or free internet to the next billion.

The birth of Mark Zuckerberg’s daughter Max seems to have focussed his mind even more on the future. He announced he’d be giving away much of his personal fortune but his campaign to provide a basic (Facebook-rich) service in India has run into bitter opposition from net-neutrality campaigners.

Less successfully we predicted that social media would play a significant role in the UK election. In the event, the politics turned out to be so dull, there was little that was worth amplifying.

2. Trends and Predictions for 2016

2.1 Mobile Trends: Glanceable Content, Bendy Phones and Personal Assistants

For many the smartphone has become not just our primary access point to digital but the remote control for life itself. iOS and Android smartphones alone are now outselling PCs 5:1 and that will rise to closer to 10:1 in the next few years. With the entry price for an Android phone is now around $35, smartphones are projected to reach around 80% of the world’s population by 2020.

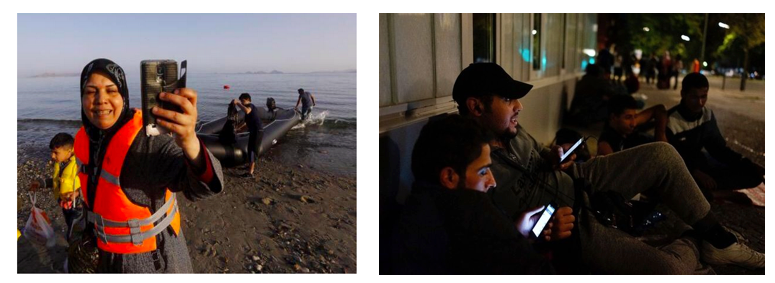

This year we’ve seen Syrian refugees use their phones to keep in touch with families, take selfies of their journeys, and plan their next moves across Europe using Google maps and chat apps.

Our phones and power banks are more important for our journey than anything, even more important than food

Wael (Refugee from Homs) 9

Pictures via Twitter

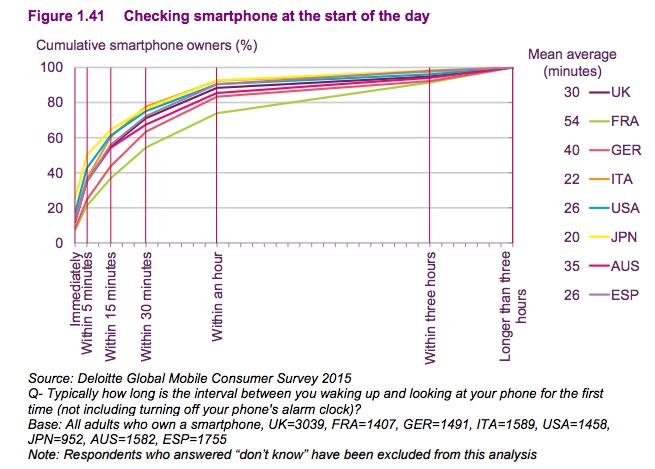

The touchscreen smartphone is only eight years old but every year we become more addicted and dependent. A recent survey showed that in the UK we collectively glance at our screens more than a billion times a day, while almost 60% of us check our mobile phones within 15 minutes of waking up (see chart below).

Here a six ways in which our dependence may develop in 2016

1. Time for an upgrade

Handsets themselves will come with lower prices, better resolution displays, faster connectivity and VR compatibility. But will it be enough to keep replacement cycles and profits up?

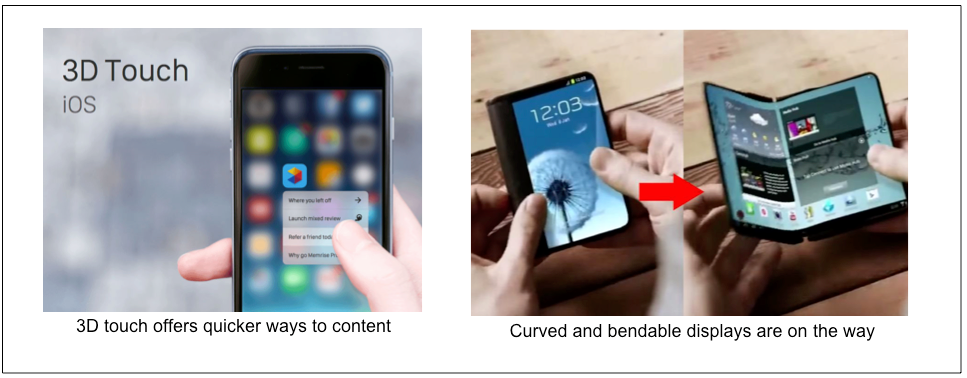

3D touch: Apple introduced a new range of interactions in 2015 using pressure to allow you to ‘peek’ or ‘pop’ quickly to get information at a glance. It’s a big deal but it won’t be clear how big until developers integrate it into popular apps this year. Rival manufactures will launch pressure sensitive displays this year.

Foldable smartphones: After years in the labs, expect to see Samsung launch a phone with bendable plastic that folds like a book to reveal a larger screen. Even if this model doesn’t stick, phones will start to get more curves in the years to come.

Waterproof smartphones: There are strong rumours that you’ll be able to take your iPhone 7 underwater or drop it down the toilet without tears.

Wireless charging: is finally showing signs of progress. It now comes as standard with latest Samsung smartphones. By the end of the year almost every phone manufacturer will include wireless charging as standard with coffee shops and bars competing for your custom with the necessary juicing stations

Tablets hit back: Sales fell in 2015 but will bounce back strongly on the back of a new generation of 2 for1 devices that double for work and play. Lighter and more powerful pro-tablets are proving a popular option in the enterprise as workers become more mobile.

Data speeds will continue to incease thanks to greater 4G roll out and upgrades to LTE-advanced and new faster Wifi standards. New services like Voice over LTE (VoLTE) are being rolled out in 2015 that will provide higher quality, more reliable calls for consumers – and lower costs for operators.

2. Virtual assistants and Zero UI

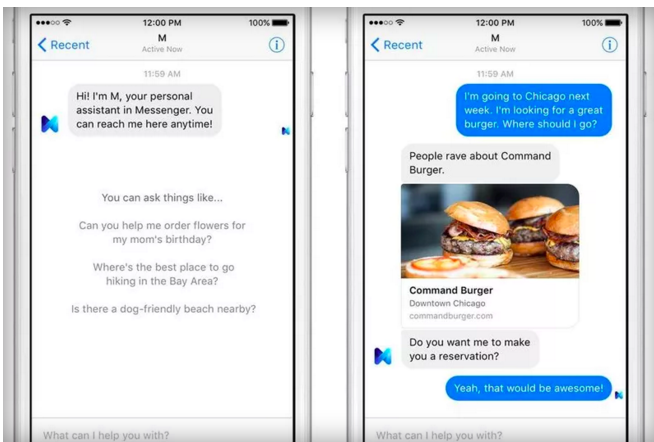

Until now, only a minority of us (20%) have been using personal assistants like Siri, Cortana, Duer (Baidu) and Google Now but this could be about to change. Facebook is entering the market with M – a tool that will sit inside its popular Messenger app – could push AI personal assistants fully into the mainstream.

Facebook M has been beta testing with a few thousand users in California

Picture credit: Facebook

M has been pitched as an easy way to find local restaurants, buy shoes (see above), access news and information but also to take on more complex tasks. This is partly because there are humans behind the scenes to take over when M gets stuck10, though eventually it is hoped that the software will learn from the humans. Partly because of its ambition, M will take years to scale and roll out globally.

AI is already proving a hit in China where Microsoft’s Xiaoice chatbot mines the internet for human conversations to enable more realistic conversations. Millions are already interacting via text using services like Weibo and the next version will include a Siri-type voice.

Deep learning and artificial intelligence looks like it will be the new frontline in the battle between Apple, Microsoft, Google and Facebook.

For publishers the main implication of AI is that they’ll have to get used to making content work not just for multiple screens but for no screens (so called Zero UI). That’s because over time more of us will talk to applications rather than touch them.

3. Push Notifications and glanceable content

With so much competition and so little real estate, the key challenge for mobile is how to attract attention. Only a small proportion of people go directly and regularly to news apps or branded mobile websites, so the role of intermediaries like Apple, Google and Facebook is becoming ever more important as a way of reaching consumers.

This is where push notifications come in, giving publishers the ability to reach out directly. Consumer use of news notifications has doubled in many countries with wearable devices like smart watches likely to accelerate the trend.

Growth in news notifications 2014-15

Reuters Institute Digital News Report 2015

The New York Times has set up a team of 11 people to specifically focus on creation and scheduling of notifications and push alerts without overly annoying and interrupting users.11

We used to be standing on a hill and shouting messages at people, [but now] there’s a growing number of users who only engage with us when we send a push

Andrew Phelps, Product Director of Messaging and Push, NYT

In 2016 publishers like the NYT will experiment with more personalised alerts (time of day, language and reading history as well as using explicit preferences such as a favourite author). We will also see more publishers appoint executives to oversee this area.

There is a generation who is not reading anything longer than a notification… Now we have journalists who are writing just notifications. The headline writers are the next generation of the successful news creator

Otto Toth Chief Technology Officer at The Huffington Post12

But even here publishers face disaggregation by the likes of Facebook Notify (currently US only13) which aggregates multiple information providers within a new app right on the lock screen – and from algorithmically driven providers like Nuzzel and SmartNews. Notifications represent both a challenge and an opportunity. The format makes it harder to monetise content and provide distinctiveness but will ultimately be critical in helping publishers drive loyalty and repeat visits to websites and apps.

4. Wearables and watches

Smartwatch adoption will gather pace in 2016 with a vast range of products aimed at every market sector. First year sales of the Apple watch have been modest but 10m offers enough encouragement to the industry that it is on the right track. There’s evidence that many consumers are waiting for use cases to mature. A recent poll suggested 25% of iOS users were considering purchasing a smartwatch in the next year14. Other providers have also been extending their range with Samsung moving into the luxury market in a partnership with TAG (below).

Many of these second generation watches are looking increasingly ‘traditional’. Here we see technology itself is becoming almost invisible – an important trend in itself.

Many of these second generation watches are looking increasingly ‘traditional’. Here we see technology itself is becoming almost invisible – an important trend in itself.

The other change is these new devices will start to be able to connect directly to the internet in 2016 rather than being tied to a phone, making applications quicker and generally increasing utility. The Apple 2 Watch will be released in the spring or early summer and include tetherless features such as inbuilt GPS along with a bigger battery.

Watches will also be able to interact directly with beacons (Apple’s iBeacon and Google’s Eddystone) to deliver highly targeted advertisements or supermarket offers

5. Mobile payments and the growth of m-commerce

Last year only 1.6% of total retail sales in the US took place on smartphones (eMarketer). But that is set to change with platform providers, retailers and marketers all having a vested interest in pushing the change. Convenience, speed and security benefits will drive adoption of digital wallets like Apple Pay and Android Pay with more retailers accepting proximity payments this year – making the process even easier.

Proximity payments should reduce friction further

Proximity payments should reduce friction further

This in itself may not be enough to persuade consumers to change deeply ingrained habits. This will only happen when coupons and loyalty schemes make it worth their while.

For publishers these trends towards frictionless payment should make it easier to entice consumers into subscriptions, membership and even micropayment – but the bigger opportunity could be in bringing together content and e-commerce (so called COMtent) a strategy being pursued by the Daily Telegraph in the UK and Gawker in the US which is reported to have made $10m in 2014 with more to come.15

6. Speeding up the mobile web

Facebook set the hare running in 2015 by claiming that news stories shared in its mobile app take an average of eight seconds to load – the slowest of all content types. Tech blogs detailed the enormous weight of many web news pages partly because several megabytes of advertising are downloaded with each story and The New York Times showed that more than half of all the data on popular news sites came from sources unrelated to articles16– costing users valuable data as well as time.

As consumers reach for their ad-blockers, Facebook and Apple see the answer as publishing content within their apps. By contrast, Google is pushing for new standards (AMP) to speed up the mobile web. Its business model depends on content being openly found via its search crawlers but it also wants a better web for consumers:

Anything less than instant simply shows a degradation, a decline in engagement

Richard Gingrass, Head of News, Google

This year expect Google to take AMP out of beta and make speed a bigger factor in its search algorithm – as well as persuading publishers to produce more content based on this standard for social networks. But publishers may be reluctant to take on another format especially as much of that content will then be hosted on Google servers.

Instead they may try to fix the problem themselves using techniques such as lazy load to stop images being downloaded until a user scrolls down the page17. They’ll also look to scale back the amount of advertising on each page and may copy ‘instant article’ features like zoom on pictures and videos that play automatically as you scroll.

2.2 Online Video Trends: Vertical, Immersive, Mobile and Social

The online video revolution is beginning to hit its stride driven by faster and more reliable connectivity and an explosion of new content. But the biggest growth in consumption will come on mobile devices with greater 4G roll out, upgrades to LTE-advanced bringing 5G-like services and new Wifi standards giving connections of up to 1.3G/s. Video is expected to grow 14x within five years and account for 70% of mobile network traffic.

Mobile data growth 2015-2021

Source: Ericsson Mobility Report 2015

Facebook’s focus on video and the growing interest from advertisers is also pushing publishers to consider expanding video output. In our survey of 130 digital leaders the vast majority said video would be a key area of focus in 2016.

What are your company’s plans for online video this year?

Source: Reuters Institute Digital Leaders Survey 2016, n=118 (excluding 12 don’t knows/did not answer)

Amongst many industry initiatives

- The BBC is closing its interactive Red Button TV service and will be focussing on a new mobile video initiative known internally as Newstream. This will build on the work of the BBC Shorts and BBC Trending teams.

- The Guardian is creating a product and engineering group around video for the first time and is a phase 1 partner for Google’s Digital News Initiative plans around video (white-label YouTube player).

- The Washington Post has put TV and video at the heart of its new newsroom with four live-shot locations.

- News Corp has bought Unruly to drive more socially relevant video for its brands and for advertisers.

- Bild and Die Welt are among German publishers stepping up video production

- The Huffington Post is expanding its video operations through content partnerships with companies like NBC; and developing Outspeak, its platform for user-generated video journalism.

- Buzzfeed is investing in a 250 strong LA based video production unit called Buzzfeed Motion Pictures to experiment with short (and long form) content. Employees test new formats such as vertical and commentary-less videos in rapid fashion using data to learn which go viral and why.18

Quotes from the survey

Producing great, digital, visual, mobile-oriented video and animation is becoming cheaper and can be integrated easier into newsroom workflows. 2016 will be the year when visual content becomes really scalable.

Anita Zielina, Editor-in-Chief New Products, NZZ

But how to do this is not always clear

Video is a difficult area for former print groups. None of us is doing it well, we do not have in-house expertise (generally) and it is vastly expensive. We will proceed with caution in this area

Prediction: Pioneers like NowThis and Vocativ that have proved they understand how to make compelling social news video will be acquired in 2016 possibly by traditional publishers looking to learn these skills.

The Reuters Institute will be publishing a detailed report into online news video in 2016.

Five other key developments to watch in online video:

1. Facebook pushes further into video

Expect to see Facebook launching a new tab just for video content (right) and better search and discovery features. You’ll also be able to float videos to allow you to watch while multitasking and there’ll be a save video for later feature.

The new video section will make it easier to integrate advertising into Facebook’s ecosystem – important if it is to encourage publishers to deliver more native video. Facebook has also been testing an enhanced ‘suggested videos’ feature, which could also offer the best opportunities for ads19.

Watch too for data and user generated tie-ups with big sports and music events to deliver a supplementary experience involving video (see IPL cricket experiments in 2015).20 Facebook could be a bidder for sports and music video rights in the future.

2. Vertical video

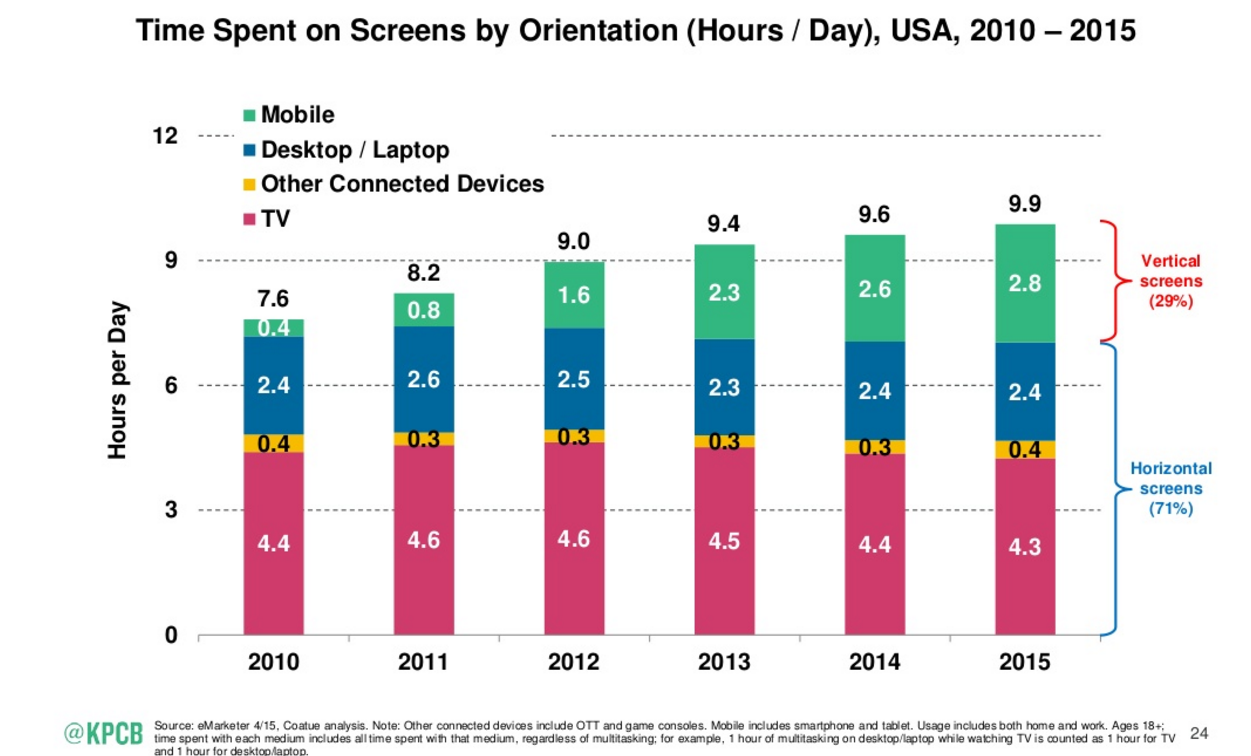

According to trend watcher Mary Meeker, almost a third of video viewing time (29%) in the US is now on a vertical screen compared with 5% a few years ago (see chart).

Time spent on screens by orientation (Hours/Day) USA 2010-15

Meeker points out that on tall screens, vertical videos simply look and work better than those shot “correctly.” YouTube reports a 50% increase in vertical uploads in 2015 while Facebook now allows for full screen playback for vertical videos. They are also the lingua franca of messaging apps like Snapchat, whose users watch six billion mostly vertical videos every day – performing, according to the company, up to 9 times better than horizontal ones.

Meeker points out that on tall screens, vertical videos simply look and work better than those shot “correctly.” YouTube reports a 50% increase in vertical uploads in 2015 while Facebook now allows for full screen playback for vertical videos. They are also the lingua franca of messaging apps like Snapchat, whose users watch six billion mostly vertical videos every day – performing, according to the company, up to 9 times better than horizontal ones.

Professionals, on the other hand, see vertical videos as the work of the devil and have been trying to educate journalists and ordinary users to shoot horizontally, but they’ll be facing an uphill battle.

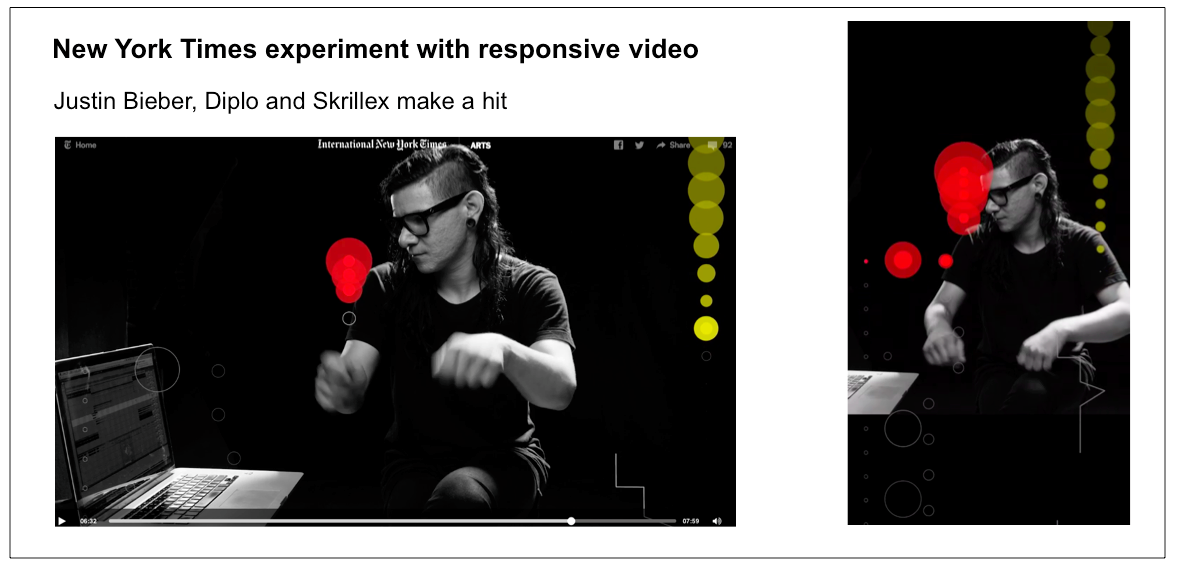

Publishers like the BBC, Mashable and Mail Online have all been experimenting with the format and we can expect to see much more professional content produced in portrait mode. Watch too for more experiments in responsive video production like the New York Times example below– allowing you to get the best of both worlds.

3. 360º Videos, VR and immersive storytelling

We’re set to be bombarded with 360º videos particularly around entertainment content this year. Facebook entered the market in September with an exclusive chase sequence to promote the latest Star Wars film where users could change perspective with the flick of a mouse or a tilt of their phone21.

Facebook has a particular interest in pushing virtual reality following its purchase of headset maker Oculus Rift. It is expected that when the Rift headset is finally released in 2016, it will support Facebook 360s producing a far more immersive experience than just interacting on screen. Meanwhile Google is promoting its own 360 approach on YouTube and with Google Cardboard handsets that integrate with existing Android phones. At Christmas it teamed up with Aaardman for an animated VR story called Special Delivery22.

In news, 360s have been deployed more prosaically to give audiences a better understanding of the devastation in Syria23 (below) and of refugee camps in various parts of the world.

The New York Times initiative to create a series of VR films and distribute 1 million Google Cardboard headsets to loyal subscribers has already created mainstream interest and we can bet on ambitious VR projects around the Olympics and US election this year24. Even so commentators think it may take time to engage audiences particularly around news.

VR and immersive storytelling have a fair amount of friction. Will a link to a VR piece entice people to strap on their Rifts or Google Cardboard viewers? I wonder if VR is the news industry’s 3D, something that gets us excited but won’t catch fire with our audiences

Kevin Anderson, Digital Strategist and a former Gannett Executive Editor

4. Scaling video on a shoestring …

Not all publishers have the time and resources to invest in teams or expensive equipment, so expect to see a host of inventive ways to keep costs down in 2016 while keeping volumes up.

- Süddeutsche Zeitung Magazin produces a range of inventive short videos for its Facebook page, which often are little more than photographs and words stitched together using free iMovie software. The consistent tone and strong messages ensure that the ‘videos’ regularly attract over 100,000 views.

- Wibbitz is software that automatically produces videos by analysing the text of a story and matching it with a mix of agency stills and video footage. The soundtrack can also be automated, though some publishers prefer to add their own human voiceover.

- NowThis, which is a leader in short-form video, deploys a workflow optimisation system called Switchboard, which recommends how to optimally construct a story on a plane crash or politics story – based on previous data. It is just one way in which NowThis producers can generate more video and scale faster.

- BBC World Service is piloting computer generated voice-overs and subtitles in multiple different languages for short online video pieces using automatic translation and synthetic voice technology25.

5. Live and social video

Faster networks, better cameras, and easy-to-use apps opened up the market for live streaming apps in 2015. But it was the integration with Twitter and the ability to summon an audience instantly through notifications that enabled Periscope to see off the competition (Meerkat and the rest).

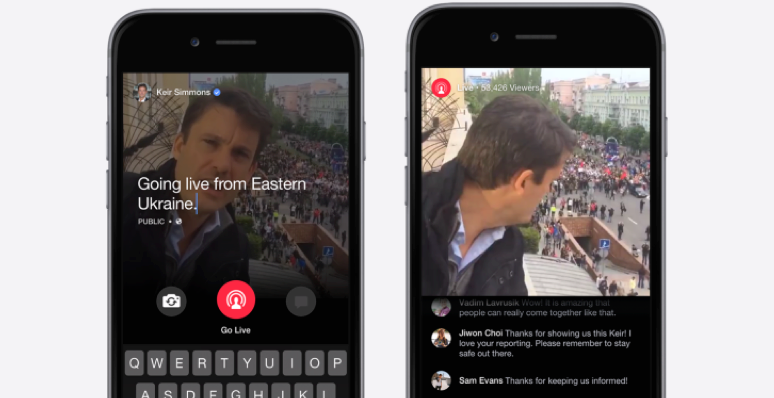

Going forward, all breaking news events will be covered with LIVE video – from multiple angles and in high definition. The decision on what to show is no longer in the hands of journalists. 24-hour news channels will ultimately need to rethink their role and responsibilities. The issue of consent – how to handle real time eyewitness media from live video streams like Periscope– is also “set to be a new ethical battlefield”, according to Damian Radcliffe at the University of Oregon.

Facebook Mentions could be next year’s big deal in live video. Using a square format to encourage comments below the video on a smartphone, Facebook Live is focussed on encouraging celebrities, politicians, journalists and other verified users to post live breaking news or behind the scenes footage with on-demand versions that stay available (unlike Periscope). Journalists were only given access to Mentions 26in September so the impact will be felt this year, not least because work posts can now go just to followers without spamming friends and family.

2.3 The Disruption of Television

The video enabled internet is not just affecting traditional online businesses but is beginning to disrupt television itself.

The amount of broadcast television watched is falling in many countries (down almost 5% in the UK last year according to Ofcom), with news and current affairs programmes amongst the worst affected. Despite this, though, we’re watching more television content than ever, on more screens and in more locations with the rapid growth of Video on Demand (VOD) and over the top services (OTT).

In the UK, two-thirds (66%) of people are now using an online service such as BBC iPlayer or Netflix to watch TV or films within the past week27. OTT and IPTV providers are also gaining ground in Europe squeezing margins for existing pay-TV operators.

Meanwhile, in the US around 50m households now subscribe to an over the top service. Consumers are starting to embrace “cord-cutting”: cancelling their cable TV service or getting rid of channels they don’t watch (see chart). Young people are referred to as ‘cord-nevers’, a group unlikely to ever subscribe to a traditional TV bundle. ESPN’s woes provided an early sign of the coming disruption28 laying off 300 jobs in the wake of falling cable revenues, increased sports rights costs and a loss of advertising to digital.

Digital subscription gains ground; Cable on the slide

Households with Pay TV vs Subscription OTT US 2010-15E (millions)

Sources: Leichtman Research Group, US Census Group, Activate analysis

While cord-cutting on a mass scale may take a few more years, the lines are blurring fast between online and television. We’re in for a year of convergence and more battles between existing operators, tech companies and content creators:

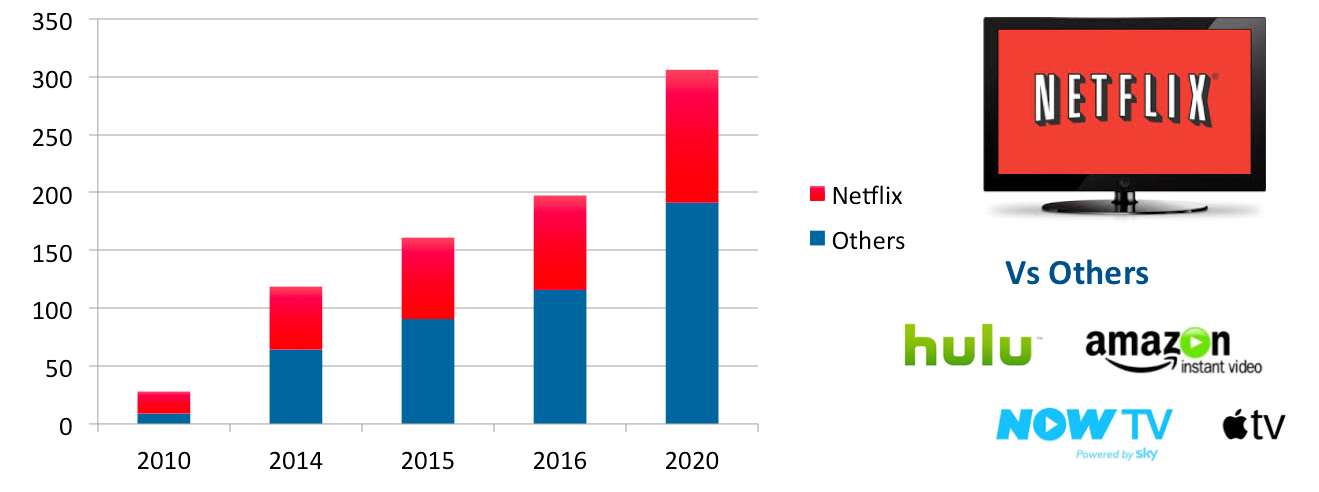

1. Big year for Netflix:

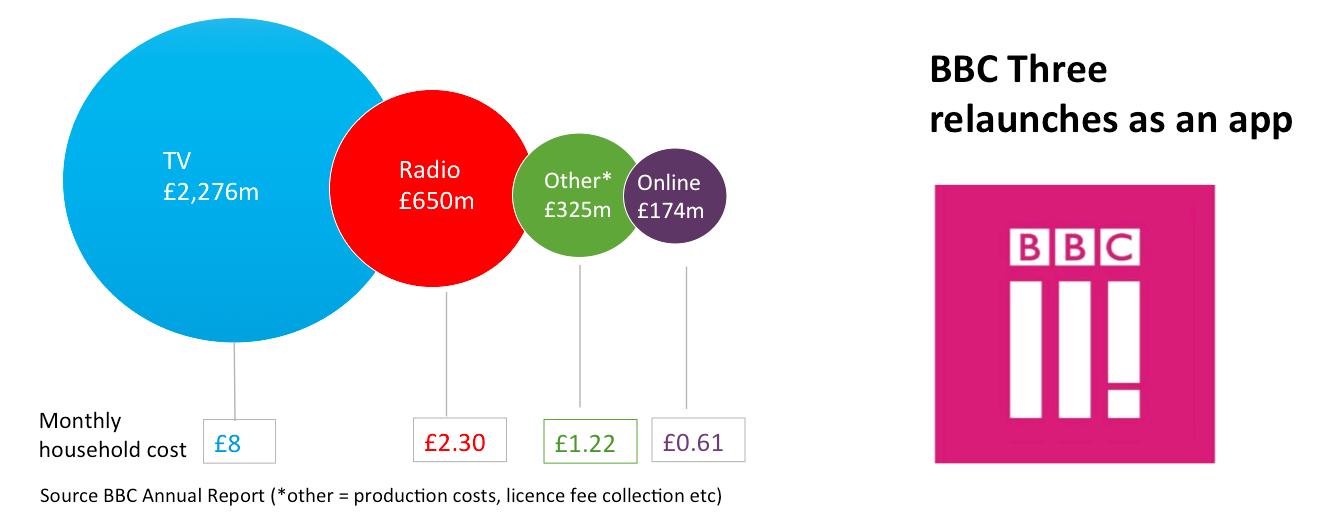

Netflix boss Reed Hastings say television sets in the future “will look like a large iPad” with an array of apps. He wants his company to be No1 app on every screen29. By the end of 2016, Netflix aims to launch in every country with a strategy of producing and owning the global rights to more original content. The company intends to invest over $6b in original content in 2016 – more than the entire licence fee funding of the BBC30.

.The market for paid for video on demand services (SVOD) is expected to double in the next few years with much of the growth coming from China and India. That would give the company revenues of around $12.2 billion by 2020, enough to invest more in region-specific content, as well as big global blockbusters.

Rise of Netflix and SVOD forecasts (million)

Source: Digital TV Research

2. Apple TV heads new OTT charge

2016 will finally see Apple launch a streaming Television service in the US after years of difficult negotiations with networks and affiliates31. With the traditional cable bundle starting to fracture, Apple’s hand has been strengthened in securing live broadcast rights and potentially one major sports deal alongside its existing SVOD offer.

Cable and satellite operators will also launch or improve their streaming services in 2016 – an insurance policy against an app based future. In the US, winners could include Sling TV (from Dish) and Go90 (from Verizon) which are open to customers from other providers.

In the UK Now TV (from Sky) remains the market leader along with apps from the main broadcasters. Watch too for more experimenting with pricing – selling individual sports games and dramas.

As more people access programming a la carte via apps, live news broadcasts could become increasingly invisible. Expect investment in new video services like NewsON in the United States a free one stop shop for discovering local news32

3. HDMI dongles that connect TVs together

We’ve got used to dongles and boxes that bring OTT content to the primary TV set or allow TVs to play content from your smartphone or tablet (Amazon Fire/Apple TV/ChromeCast) but now expect pay TV providers to reverse-engineer the process. We could see them offering dongles that extend their service seamlessly to other TVs around the house. It’s a logical way of protecting against more cord cutting by delivering extra value for the existing package.

4. New video ad metrics and cross device selling

Given video’s growing importance in terms of content and advertising revenue, we will see calls for consistency around viewability metrics in 2016 around VOD (Video On Demand) to allow comparability between online and television.

Definition of video views remains problematic

Source: Various

The key metric for a video ‘view’ varies from 3 seconds for Facebook to 30 seconds for YouTube while the IAB classes a viewable advertisement at just 2 seconds of continuous play33. This makes it hard to compare the relative effectiveness of the different platforms. It also doesn’t match what the industry has come to expect with television where most ads are watched right to the end.

This year will also see the start of cross device advertising. Logged in VOD services, and better tracking technology will allow advertisers to target individual users as television starts to behave more like the web. For example it will be possible to show sequential ads to the same person over time, unlocking new creative advertising possibilities.

5. Public Service media under threat

The explosion of new media channels and the move to online is putting public broadcasters under pressure as never before. With audience share declining it is harder than ever to maintain support for universal taxation or licence fees. The BBC will come through its charter renewal but not before a further assault from the UK’s newspaper sector over the dominant role of its online news site.

Another milestone in 2016 – the licence fee link with the television set will end, closing a loophole that made it possible to watch on-demand television on laptops or smartphones without paying but television services will still face significant cuts including the potential axing of the BBC News channel34.

2.4 Podcasting and Audio Boom

While video continues to lead the way, audio is undergoing a revival driven by connected smartphones and its multitasking friendly format. In the US, Barack Obama made his podcast debut on WTF With Marc Maron and Serial announced an exclusive distribution deal for its second series through Pandora.

The move from download to streaming consumption is changing the economics of podcasting, opening up the possibility of higher revenues through targeted advertising and dynamic ad insertion. Companies like Acast and Panoply will be rolling those solutions out this year.

Currently only around 17% of Americans listen to podcasts and that partly because of a longstanding discovery problem with over 30,000 regular programmes made each week. Tools like Clammr could make it easier to share snippets from longer podcasts through social media, while NPR National Public Radio has launched Earbud.fm, a curated podcast recommendation website and app. Meanwhile Spotify will be incorporating podcasting in 2016, potentially opening quality speech audio to a much wider audience.

2.5 Social Media and Messaging Apps – What Next?

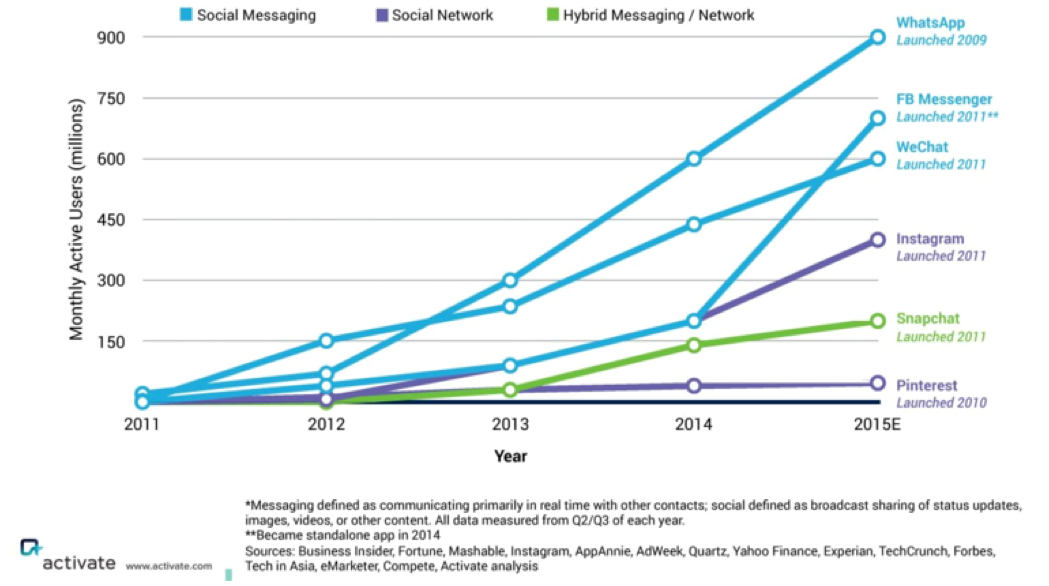

Social media and messaging apps became more central to more people in 2015. Facebook reached a billion users a day for the first time, Instagram broke through 400 million users and despite its difficulties, Twitter still reaches around 350 million active users each month.

Meanwhile users have been migrating fast towards messaging apps because in many countries they offer a no cost or low cost alternative to SMS. Now these new digital giants are working out how they can capitalise on these enormous user bases to take on Facebook with new services and functionality.

Rapid growth of messaging and hybrid networks 2011-2015

The key focus in 2016 for both messaging apps and social networks will be to get us to spend more time within their apps. That means insourcing more content and reducing friction with other services so we neither want, nor need, to leave.

Apart from the continued focus on video and the growth of live streaming (already covered above), here’s what else we can expect …

1. Rise of long-form social content

Instead of linking to articles and blogs, social platforms will encourage publishers and marketers to publish natively within their platforms. Some Instant Article functionality will also be incorporated within a revamped Facebook Notes as the network looks to reward content that engages readers for longer.

Under pressure, Twitter will increase its 140-character limit and encourage postings of up to 10,000 characters changing the nature of the platform and putting it in direct competition with Facebook, LinkedIn and Medium. But this is just the start of a trend that will see more content created, distributed and monetised through social platforms.

The individual website won’t matter …It will be about getting it [news] from centralized websites.

Evan Williams, Founder Medium (speaking at I-Squared Publisher Summit)

In 2016, strategist Jonathan Marks says we’ll see more people subscribe to long-form investigative journalism through sites like Medium and a market will develop for those who curate the content on those platforms into coherent collections such as https://medium.com/backchannel.

2. Growth of social e-commerce and new in app service

Buy buttons on sponsored posts have been around for a while but the range of frictionless options to spend money will grow markedly this year.

Pinterest will be looking to build on its success with buyable pins (1),Twitter is experimenting with in platform sales (2) while Facebook has expanded options for non-profits (3) – allowing donations and campaign pages to be run without ever leaving the platform.

Asian networks like WeChat and Line (see below) have gone even further integrating payment services, taxi booking, news and even music services.

Asian networks like WeChat and Line (see below) have gone even further integrating payment services, taxi booking, news and even music services.

By the end of 2016, most social media brands will have launched more services or done a better job of integrating existing services like Uber and Spotify. The bottom line is that we’re likely to be spending more time and more money with social and messaging platforms in 2016.

3. Chat apps make presence felt in breaking news

Over the past year more eyewitness pictures, videos and comments have emerged through platforms like WhatsApp, Line, WeChat and Telegram – rather than just Twitter or email. Some of these apps will enable APIs this year which will make it easier for news organisations to distribute content something that has been hard until now.

In this respect, perhaps the most interesting to watch will be Snapchat’s approach to news. It’s been trialling approaches to breaking news with Live Stories and last year’s much praised coverage of the San Bernardino massacre.

A number of news organisations have been experimenting with its Snapchat Discover section, including the Wall St Journal, the first business publication. The journal has a five-person team dedicated to creating Snapchat content, publishing eight items a day.

From the Survey

Reaching new audiences on platforms like Snapchat with 100 million daily engaged users – that’s a huge opportunity

Sarah Marshall, Wall St Journal

Snapchat has moved fast since its beginnings as a pioneer in the ephemeral-image-sharing genre, to a slightly-less-ephemeral storytelling app, to a host of branded content ‘channels’, to a publisher in its own right based on curation of geofenced UGC.

As Paul Bradshaw points out: “Where Twitter’s innovations sometimes feel like a platform on the back foot, Snapchat feels like it’s a step ahead of where everyone assumes it is”. Having said that Paul is not alone in wondering if the Snapchat bubble will burst in 2015: “so far it has got by without any hard metrics for publishers. That can’t last.”

2016 could be a make or break year with others predicting Snapchat will go public this year35

4. More secure chat apps

With government snooping and concerns about personal privacy on the rise, we can expect to see greater adoption of encrypted and secure networks 36 Telegram has become popular in the Middle East with ordinary people but also with groups like ISIS, which use it to communicate and disseminate propaganda, Telegram has ‘secret chat functionality’ that uses end-to-end encryption, self-destructing messages and leaves no trace on servers.

Firechat is another app that became popular during the Hong Kong protests in 2014 and it uses the Bluetooth connectivity and radio aerials on phones and smartphones to create a “mesh” network of people in the same area. It has plans to develop the platform this year and has introduced private messaging.

Yik Yak and Jott are also growing fast with university and school age children in the US as they both specialise in anonymous and secure messaging.

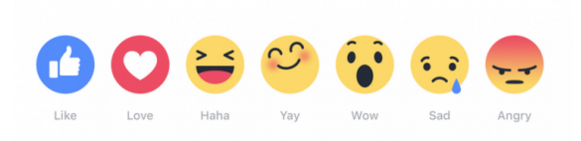

5. More emotional sharing options

Twitter replaced its ‘favourite’ symbol with a heart in 2015 just as Facebook was laying plans for a more varied set of emotional responses to content that are being tested first in Spain and Ireland.

“What [people] really want is the ability to express empathy. Not every moment is a good moment.”

Mark Zuckerberg, CEO Facebook

Hearts and likes are often seen as inappropriate for news stories that engender a complex set of emotions – such as natural disasters. These new options provide more nuanced ways of sharing as well as providing useful feedback signals for news organisations and brands about how content is going down with audiences.

Hearts and likes are often seen as inappropriate for news stories that engender a complex set of emotions – such as natural disasters. These new options provide more nuanced ways of sharing as well as providing useful feedback signals for news organisations and brands about how content is going down with audiences.

Other possible signals around content in 2016 could be more buttons to help verify truthfulness and accuracy, given the extent of hoax pictures and posts in recent news events. Expect at least one traditional news organisation to experiment with emojis and integrate them into the app experience.

6. Social at work

This could be the year the workplace truly begins to harness the power of social for internal purposes. For years, intranets and knowledge management software has failed to join the dots within complex organisations while email has been clogged up with social conversation. Now simple cloud based services are changing culture and productivity within the enterprise.

Tools like Slack and Hipchat are leading the charge helping teams share and organise information, allowing people to come together in groups in a non-hierarchical way.

From the survey:

This tool (Slack) has completely changed how my teams interact with each other, and has had a similar effect in the newsroom – completely though organic adoption rather than any specific concerted effort

In 2016 the recently launched Facebook at Work will bring these approaches to mainstream audiences such as workers at top UK banking giant RBS37. The interface is almost identical to the home version although personal and professional accounts are kept separate and you ‘follow’ rather than ‘friend’ colleagues.

2.6 Online Advertising: The Year of the Ad-Apocalypse?

With over half of all advertising spend going online this year in many countries (UK), there’ll be intense focus on where that money is going and how effectively it is being spent. Marketers and publishers will be trying to take advantage of advances in audience targeting and big data capabilities while agencies and brands will look to up the quality and creativity of their messaging.

But consumers are in boisterous and resistant mood. They are increasingly sensitive about their privacy and are primed with powerful ad blockers like AdBlock Plus and bug tracking tools like Ghostery.

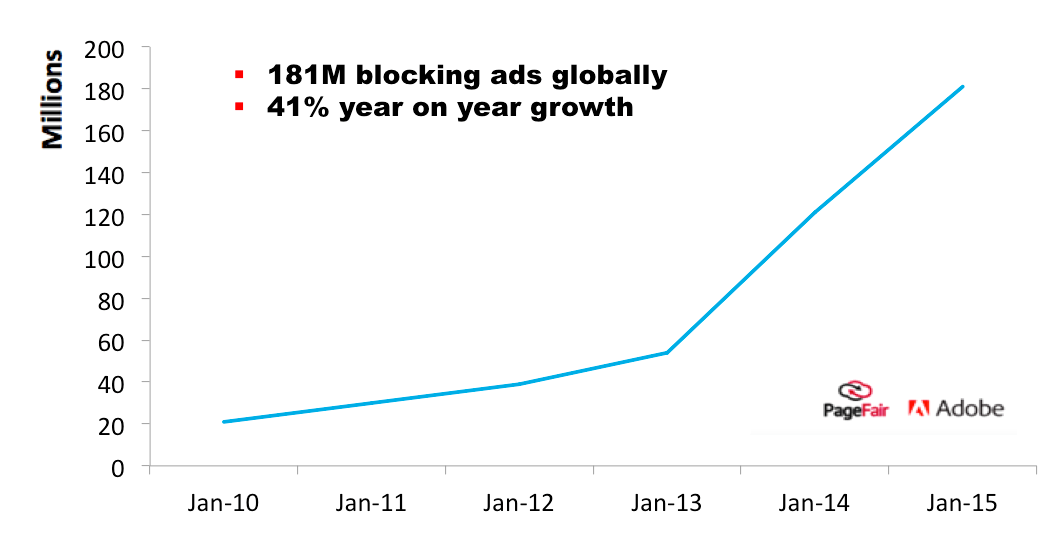

A YouGov survey in Nov 2015 showed 20% ad blocking in the UK, but double that (40%) for 18-24s38. So far this has mostly been confined to desktop but in 2016 we’ll see this move to the mobile mainstream following Apple’s decision to open up the iOS platform to ad and content blockers.

Global Growth of Ad-blocking 2010-2015

Source: Adobe/Page Fair Ad Blocking Report 2015

Perhaps the biggest threat of all comes from Israel-based mobile ad blocker Shine, which is working at the network level to stop all advertisements. This ‘ad apocalypse’ is already happening in Jamaica 39where one small carrier, Digicel has signed up and is blocking all display, video and in app ads. It is offering Google, Yahoo and Facebook a revenue share deal on ads it lets through. If bigger mobile carriers go down this route, the game changes significantly.

But ad-tech is facing a host of other problems too including Ad fraud and viewabilty.

The extent of ad fraud only really came to light in the last 18-months with a series of well-researched studies 40 suggesting that total fraud in the US amounted to around $6.3bn (20% of total advertising spend). The Association of National Advertisers (ANA) showed that software bots – not people – viewed 11% of display and 25% of video ads.

Advertisers are particularly concerned about the implications for reaching millennials. This is the group most likely to use ad blocking, least likely to own a television and most likely watch programmes (ad free) through Netflix or BBC iPlayer on their laptops or phones.

We’re at risk of bringing up an entire generation in a world without advertising.

Jon Block VP of Platform and Product at Videology

This is both a problem and an opportunity; it is recreating scarcity that could allow publishers who can successfully deliver viewable ads to millennials to charge higher premiums.

The volatility in this area makes predictions particularly hard but here’s an attempt:

- Ad blocking wars: Expect more publishers to follow the example of Axel Springer which forced users of the Bild website to turn off ad blockers or pay a monthly fee to continue using the site. It says over two thirds complied and usage is now in single digits. The Washington Post has also started redirecting readers to a subscription page or asks them to sign up for newsletters. But the ad-blocking companies will strike back trying to intercept these messages and turn them off.

- More legal and regulatory moves: As the economic impact becomes clearer, publishers will try to get regulators and legislators to take action. They will argue that ad blocking is undermining the existence of professional journalism and if courts won’t close them down the law must be changed. In response, the blockers will argue that advertisers and publishers are invading privacy, spamming mobile users and draining mobile data.

- Ad blocking goes mobile: So far, awareness of ad blocking on smartphones is low but with consumers increasingly sensitive about privacy and data charges the rates could match desktop by the end of the year. This will come from mobile apps like Crystal and from new ad blocking browsers like UC browser, which is sweeping through countries in India and the Far East where high data charges are a big issue.

- Facebook, Google and Apple will remain immune: The big tech companies will find a way to buy off or neutralise ad blocking within their apps and through mobile initiatives like AMP, Instant Articles and Apple News. In turn, this will drive the trend to publishing via distributed platforms with a limited set of advertising slots and formats – giving yet more control to Google and Facebook.

- Ad-tech fixes to get round the ad-blockers: We’ll see more advertising moving to video, which tends to be harder to block because it involves fewer calls to third parties. Publishers will also change the way they serve conventional display ads using server-to-server calls rather than front-end code.

- Advertising quality improves: Brands and agencies will be pushed to create advertising and marketing messages that engage rather than interrupt consumers. Good recent examples include two puppyhood ads for Purina carried by Buzzfeed.

The problems of ad-tech are severe and will take many years to solve. But out of the chaos we’ll start to see better ads and approaches that successfully generate revenue at the same time as respecting consumer user experience.

2.7 Publishing and Journalism

In our Reuters Institute digital leaders’ survey, respondents were not as downbeat as might be expected about their business prospects in 2016. A number of those without solid digital revenues or who relied on digital advertising were more worried than last year (22%) but some with paid content or mixed business models were largely less worried (20%) or equally worried (50%) compared with last year.

To what extent are you worried about your company’s digital revenues?

Reuters Institute Digital Leaders Survey 2016 n=119 (11 did not answer this question)

To some extent this data reflects the steady progress many publishers have made in generating digital revenues, but it also indicates a lack of urgency still felt in many European countries (like Austria and Switzerland) where consumer behaviour is changing more slowly and print revenues remain strong.

Even so, a number of respondents expressed concern about the new dynamics of mobile – in making it more difficult to make money than even desktop – and helping tech platforms get even stronger:

Mobile audiences grow at pace but the dynamics of mobile advertising are different to what we’ve experienced before. What growth there is in the market is being won by Google and Facebook. (anon)

Across our respondents there was a strong consensus on the need to diversify revenue streams to replace declining advertising revenue and to contingency plan against increased ad block usage. A number of respondents talked specifically about moving the focus away from page views and display ads in 2016.

In that regard, we can expect to see:

1. More crowd-funding and membership schemes:

The Spanish news site El Espanol raised a staggering €3.1 million ($3.4 million) through crowd-funding in less than two months. Other European start-ups have raised over €1m including De Correspondent in the Netherlands and Germany’s Krautreporter. National Public Radio in the US and Wikipedia have demonstrated the power of regular funding drives and expect to see the Guardian look to scale its membership scheme globally using similar techniques mixed with premium content offers.

2. Subscription innovation and micropayments:

Blendle, the self-styled ‘iTunes for journalism’ will launch in the US in early 2016. It has backing from the New York Times and Axel Springer amongst others and has already signed up 550,000 subscribers in the Netherlands and Germany for a service where consumers pay a fraction of a euro per article – and can get refunds if they are disappointed with the content. Given the failure of low cost subscription services like NYT Now, paid content providers see these services as a potential source of additional income from users who would never sign up for a full subscription to just one outlet. Elsewhere watch for innovation on subscription such as the Boston Globe’s 99c a day approach 41 and the growth of price discrimination.

3. The rebirth of COMtent for a mobile age

Mixing content and commerce can be an important revenue source for publishers focused on preserving editorial integrity. More seamless users journeys and frictionless payment are opening up new possibilities that were never possible in print or even via a computer. Get the look fashion features, gift guides and product reviews can be reborn in a mobile context where users can be sent vouchers or advised on nearby locations for the best deal.

Beyond Clicks and Views and Towards Engagement

Over half of our publishers said increasing levels of engagement (54%) would be top priority in 2016, although in most cases this was often balanced with the need to drive greater reach.

From the survey:

We saw record of numbers of readers coming to us in 2015. In 2016, our biggest opportunity is to turn that interest into a more deeply engaged audience

Julia Beizer, Director of Product Washington Post

Top strategic priorities for 2016

Reuters Institute Digital Leaders Survey 2016 n=123

The Year of Audience Engagement

The focus on engagement is partly related to the increasing need to drive quality traffic but the move to distributed content has also focussed minds on how to engage users in third party platforms like Facebook and Google42.

For all these reasons most big publishers are investing in better analytics and understanding of data and have been setting up new teams centred on audience engagement. The BBC and the Financial Times were amongst publishers joining this trend in 2015 and will be hitting their stride in 2016.

[This] will be the year that we begin to understand what success really looks like, and realize that it takes as many different forms as there are different audiences on different platforms.

Renée Kaplan, head of audience engagement at the FT43

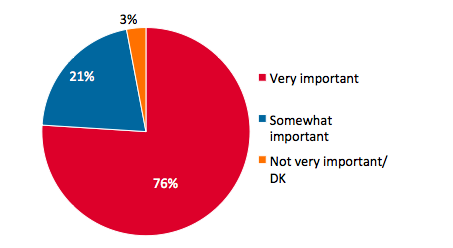

This new complexity is recognised in our survey where over three quarters (76%) of respondents said that it would be critical to improve the use and understanding of data in the newsroom this year.

How important will it be to improve the use data in the newsroom in 2016?

Reuters Institute Digital Leaders Survey 2016 n=123

Around two thirds of publishers who responded to our survey (65%) had deployed Chartbeat in their newsrooms to provide real time feedback. 15% were using NewsWhip, a specialist tool for understanding how content is performing in social media, and almost half (45%) had also built their own home-grown systems to help understand how content was being used.

Beyond new business models, data and video (covered above) what other journalism trends can we expect in 2016?

1. Renewed importance of publisher apps

Despite the rise of distributed content, most revenue will come from repeat visits from loyal customers. In a mobile age this increasingly means apps for four key reasons.

- Apps will largely be protected from ad blocking. It is in Apple’s interests to ensure the health of the app economy vs the open web.

- App content is now visible (it can be indexed by search since the iOS9 release) and automatically linked with web content. Publishers can ensure regular users always get a consistent experience wherever they come from.

- Speed and performance will remain critical on mobile devices. Native apps will always beat the open web.

- Apps provide always on identification and unlock the power of notifications to drive more repeat visits.

2. Importance of partnerships and scale

Distributed content, global platforms and mobile personalisation demand more scale and involve more complexity than can be provided by any individual publisher. This explains the partnership strategy of the Huffington Post (now teamed with local providers in more than a dozen countries) along with the international expansion of the Buzzfeed, Business Insider and even the New York Times.

The pace of change means that new skills can’t be grown quickly enough internally – hence Axel Springer’s investment strategy in companies like NowThis to help provide short form video and Nikkei’s purchase of the Financial Times for English language reach.

Publishers are also beginning to realise that they will need to work together more (e.g. Pangaea advertising alliance 44) as well as with tech giants like Facebook and Google. They may never be best friends but the last year has shown that the big US companies are prepared to listen more – for example with Facebook rethinking the monetisation of instant articles, Snapchat enabling deep linking of stories and Google through its Digital News Initiative. All sides in their own way have an interest in ensuring high quality content continues to be worth producing. On the other hand, the proliferation of platforms is straining publishers’ limited resources, so they’ll need to be choosy about exactly where they place their bets.

3. Focus on utility and distinctiveness

The growth of visual journalism has been good for attracting attention but not always for driving value (and hence revenue). This year, expect to see a growth in tools that focus on solving problems and answering questions along with more unique content.

This might involve answering reader search queries such as: ‘How tall is David Cameron?’ as the Guardian did during the UK general election or creating data and editorial tools that help people make decisions around what to eat, where to go to university or how to spend time more profitably.

For paid content sites much of this will focus on ways of making proprietary data more useful and accessible to subscribers but we’ll also see a renewed focus on creating more distinctive content in order to stand out from the crowd.

Even digital born companies like Buzzfeed are investing heavily in original journalism, realising that it isn’t enough to “just crib and reshare in an echo chamber”45.

Linked to these new objectives, we’ll also see new ways of trying to measure utility or value rather just views or even engaged time. NPR is focussing on completion rates for its visual stories and is developing a carebot to look at value 46. Others are going further trying to understand impact of stories and coverage over time.

4. Robo-Journalism

Until now, most innovations have centred on the distribution not the creation of content but advances in pattern recognition and natural language generation are changing that.

Software from companies like Automated Insights and Narrative Science are already being used to create automated earnings reports for The Associated Press and sports reports for companies like Yahoo!. In tests of simple stories, readers couldn’t tell the difference between those generated by an algorithm and by journalists47. Twitter bots are already churning out thousands of 140 character updates on stories of public interest such as seismic activity in California (below) and the Washington Post has been experimenting with bots in engaging young users with quizzes and games on the chat app like Kik48.

Journalism based on data collected by sensors, cameras and drones also has the potential to reinvent local journalism in terms of weather, traffic and local events sourced from social media. It may not be long before we see the emergence of automated content farms that rewrite popular trending copy from multiple sources and we’ll also see more cyborg journalists in newsrooms; helpful robots built into CMSs that automatically bring in facts, references and links to support stories49

2.8 Start-Ups to Watch

Here are ten companies we may be hearing more about in the next year.

1. Symphony: is a social network for Wall Street with a mission to revolutionise the way bankers and financial specialists communicate and share information. Think Slack with extra security. In the enterprise, these personalised systems also help distribute key financial news and Wall St Journal Chief Innovation Officer Ed Roussel believes Symphony’s “network of arteries will eventually be driving the lifeblood of Wall Street”. It has large financial backing and a waiting list of content providers wanting to integrate with their platform. All they need do is improve the usability of the product to start having a serious impact49

2. Brigade: Started by Napster cofounder Sean Parker, Brigade is a US platform that encourages civic action and empowers users to seek change.

Users are prompted to answer questions that help match their views with political candidates and advocacy groups. They can also try to persuade others to change their positions on issues – for which they get scored. The 2016 US election will be the first big test for the platform which also offers parties and political organisations a dashboard of who is supporting their issues and what is trending in the news.

Users are prompted to answer questions that help match their views with political candidates and advocacy groups. They can also try to persuade others to change their positions on issues – for which they get scored. The 2016 US election will be the first big test for the platform which also offers parties and political organisations a dashboard of who is supporting their issues and what is trending in the news.

3. Vervid: This app is all about experimentation with vertical video – creating compositions that make sense for screens that are held upright 94% of the time. Vervid also features profile images that ‘burst’ into life as video thumbnails.

4. Newsflare: is an online video news community and marketplace for user generated video content. It supplies video to over 200 news organisations and rewards contributors with recognition, privileges and financial rewards. It aims to cover news that is too remote or too local for many traditional news organisations. In 2016 it is expanding into China.

5. Gimlet: is a fast growing podcast company built on the success of a show called startup, which documented founder Alex Blumberg’s (ex This American Life) attempts to set up his own podcasting network. Gimlet Media (as it became) went on to raise $1.5 million in funding, $200,000 of which came from a crowdfunding and launch as series of high quality podcasts that are defining the medium.

6. The Quint: Is an Indian mobile first news site in English and Hindi founded by entrepreneur Raghav Bahl the man behind media group Network 18. It’s looking to bring a fresh modern tone to coverage of serious and lighter issues. The site is built on a new digital publishing platform called The Quintype, which not only publishes stories but uses predictive analytics for scheduling articles, builds in social media management and contains an integrated ad engine.

7. Ola (also India): This taxi-hailing app is a reminder that US companies like Uber will face stiff competition in many Asian markets. Ola is expanding to cover around 200 cities on the back of rising mobile connectivity in India. It is the third-most valuable venture-backed company in India with a valuation of $2.4bn.

8. Leap Motion: is a controller that provides a new way to interact with a computer or mobile device. You can point, grab, pinch or punch your way to navigate through the digital world.

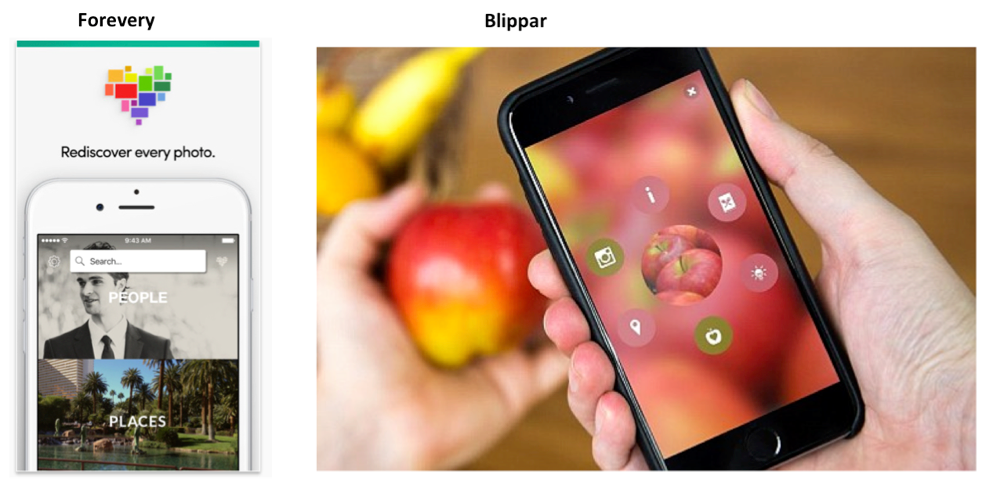

9. Forevery: One of a host of apps incorporating image recognition technology to help you search for people, place or things in your mobile picture library. No tagging is needed as the app can also be trained to recognise members of your family or specific objects. (see also Google photos).

10, Blippar: Is an image recognition and augmented reality mobile app that aims to change the way we search for things and interact with the world around us. It identifies and categories items in the camera’s field of vision offering links and opportunities to interact.

And watch too for Platfora (extracting value from big data), Infinario (for publishing analytics), Relsci (a platform for mapping relationships with people in the news), Immersive.ly (for VR news production), and the reinvention of Upworthy.

2.8 Five Technologies that May Shake Our World

1. Virtual reality

After all the hype, this is the year when consumers will start to get their hands on new headsets and experience fully immersive content. The HTC Vive will join Sony’s PlayStation VR and Facebook’s Oculus Rift headset on the market in the next few months amid huge publicity. But it will be cheaper systems like Google’s Cardboard VR headset, where you slot in an Android smartphone,that will provide most people with their first virtual reality experience.

Initially the main focus will be games and adventure experiences such as Everest VR, which will be part of the Hive release. Created by Icelandic studio Solfar, it uses a technique called photogrammetry to stitch together over 300,000 high photos to hint at a new genre of experiences, somewhere between filmmaking and gaming.

Initially the main focus will be games and adventure experiences such as Everest VR, which will be part of the Hive release. Created by Icelandic studio Solfar, it uses a technique called photogrammetry to stitch together over 300,000 high photos to hint at a new genre of experiences, somewhere between filmmaking and gaming.

Longer term, there are potential applications in education, medicine and news (discussed earlier).

Virtual reality will be a new multi-billion dollar industry with opportunities for many players from content makers to headset manufactures. Yet again Facebook and Google are set to be the big winners – controlling the full spectrum of assets needed for success: hardware, software, content, talent, distribution networks and advertising.

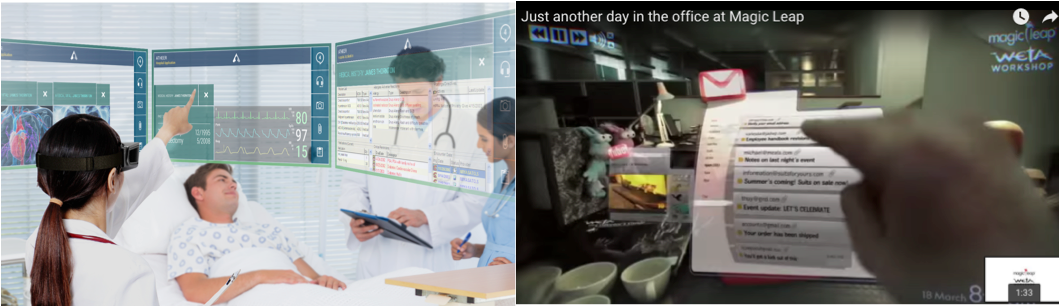

2. Augmented reality

While VR is about immersive experience, mixed reality is about adding information to what we see in the real world. The Microsoft HoloLensis a smart glassesheadset that is also a self-contained Windows 10 computer. It uses advanced sensors, a 3D display and spatial sound to allow for augmented reality applications. Users interact using their eyes, voice or hands. Manufactures like Samsung have expressed interest in building products on top of the HoloLens.

Other pioneers like Atheer have refocused efforts on the millions of workers who need to keep their hands free but may also need access to information or data (see medical example below). Google Glass is also being redeveloped for the enterprise market.

One other big mover in 2016 is expected to be Google backed Magic Leap, which has produced a series of impressive videos showing consumer use cases relating to entertainment and the office (above right). Magic Leap has raised over $1.4b in funding and now says it is moving out of R&D into production.

3. Next generation drones

Consumer sales are expected to reach four million this year and 20 million by 2020 – with most drones equipped with high definition cameras. In the US, the Federal Aviation Authority (FAA) is requiring users of unmanned aerial devices to register units by the middle of February, a move which suggests that the serious business use of drones is getting nearer.

Full commercial services are probably still a few years away as a number of legal and technical hurdles remain to be overcome. These include concerns about personal privacy, safety as well as the potential use of drones for terrorism.

At least two near misses have been reported by commercial pilots landing at UK airports – while footage of a falling drone narrowly missing an Austrian skier was widely shared over the internet51.

Manufacturers will be demonstrating new flight safety features involving geo-fencing to ensure drones stay away from designated areas. Software from companies like DroneDeply will also ensure drones avoid obstacles in the skies as well as when landing.

Amazon is continuing to improve and test its prototype delivery fleet – Amazon Prime Air. In a company video, Jeremy Clarkson showcased the latest features of its drone, which will eventually deliver packages in less than half an hour to a designated drop zone outside your house. Expect more retailers to announce drone delivery programmes in 2016.

Meanwhile news outlets including the Washington Post and CNN are taking part in a research programme with Virginia Tech on a site that has been officially approved by the FAA52. They’ll be experimenting with new uses for drones filming breaking news, gaining new perspectives and verifying information. And expect Twitter to move into tweet controlled drones, following a patent application in December for a UAV that takes photos and videos that can be shared on user accounts53.

4. Internet of things

The number of physical devices connected to the internet continues to rise exponentially. That means new screens like wearable technology or the smart screens that can display information from the internet – but also more devices with sensors built in that allow services to be optimised and improved in real time.

Smart mirror display: Virtual fitting rooms, style advice and weather information

Smart mirrors like the one above come with 3D camera technology that turn them into a virtual fitting room helping people see how they look in clothes, shoes or jewellery – before buying.

Smart mirrors like the one above come with 3D camera technology that turn them into a virtual fitting room helping people see how they look in clothes, shoes or jewellery – before buying.

Even lightbulbs are getting a makeover. Phillips Hue connected lighting allows you to change colours or moods to match your mood or to programme lights to come on or off using your smartphone.

The implications for business and public services are potentially even more powerful. More and more devices from driverless cars to traffic lights to thermostats come with sensors built in that allow services to be controlled and optimised remotely in real time.

With these new capabilities will come new dilemmas and debates about the extent to which we are losing the ability to think for ourselves and about the security implications of having all this data being sucked out of our homes and delivered to outside companies or individuals.

5. Virtual currencies and the Blockchain revolution

Bitcoin’s rollercoaster ride suggests we need a deeper level of trust before ordinary consumers are willing to commit their money to currencies that are not backed by banks or ultimately a nation state.

The technology behind Bitcoin is cryptographic system called Blockchain, which can verify transactions without the need for a trusted third party.

The technology is still in its infancy but this year we’ll start to see Blockchain used for much more than just money

Blockverify is a start-up that provides traceability for high-value items like diamonds. It would allow you to prove your diamond ring is ethical for example54.

Deloitte is experimenting with distributed digital ledgers using blockchain, PeerTracks and Bittunes are shaking up digital music, while Verisart is working on ways to improve how art is tracked and verified55.

There are clear possibilities for using the same process to manage news videos, pictures and other intellectual property in a shared and distributed world. Crypto-currencies and the systems that underlie them have huge potential to disrupt long-standing industries but will ultimately reduce transaction costs and improve security for all of us.

About the Author

Nic Newman is a Research Associate at the Reuters Institute for the Study of Journalism and has been lead author of the annual Digital News Report since 2012. He is also a consultant on digital media, working actively with news companies on product, audience, and business strategies for digital transition. He has produced a predictions paper for the last ten years, though this is the first such paper to be published by the Institute.

Nic was a founding member of the BBC News Website, leading international coverage as World Editor (1997–2001). As Head of Product Development he led digital teams, developing websites, mobile, and interactive TV applications for all BBC Journalism sites.

Acknowledgments

The author is grateful for the input of more than 130 digital leaders from more than 25 countries that responded to a survey around the key challenges and opportunities in the year ahead. Respondents came from some of the world’s leading traditional media companies as well as new digital born organisations. Survey input and answers helped guide some of the themes in this report quotes and data have been used throughout. Some quotes do not carry names or organisations, at the request of those contributors.

The author is particularly grateful to a number of other experts who were interviewed for this report, responded by email or offered other support or guidance: Kevin Anderson (ex Gannett executive), George Brock and Jane Singer (City University), Paul Bradshaw (Birmingham City University), Richard Sambrook (Cardiff University), Jon Block (Videology), James Haycock (Adaptive Labs), Damian Radcliffe (University of Oregon), Andy Kaltenbrunner (Medienhaus Wien), Jonathan Marks (CEO Critical Distance), Bertrand Pecquerie (CEO Global Editors Network), Trushar Barot (BBC), Kevin Hinde (Macmillan), Neil Sharman (consultant).

Also thanks to the team at the Reuters Institute for input and support including David Levy, Rasmus Kleis Nielsen, Federica Cherubini, Annika Sehl, Alessio Cornia, Richard Fletcher and Antonis Kalogeropoulos – as well as Alex Reid, Rebecca Edwards and Hannah Marsh.

As with many predictions reports there is a significant element of speculation, particularly around specifics and the paper should be read with this in mind. Having said that, any mistakes – factual or otherwise – should be considered entirely the responsibility of the author who can be held accountable at the same time next year.