In this section we draw on country data on brand performance along with questions asked elsewhere in the survey about the types of news sources accessed online and offline. This includes a typology of different online sources whether they are traditional newspaper providers such as the New York Times, broadcaster websites like NHK, Globo, and the BBC, or digital-born players like Yahoo, Huffington Post, or BuzzFeed.

In the chart below we have used these classifications to show the relative balance between these groups in a few selected countries, in terms of weekly consumption.

In the US, Canada, and particularly the UK, broadcast brands take the largest share, with newspapers playing a lesser role. In Finland and Spain and to a lesser extent Germany and France, it is newspaper brands that have made the running in digital news. By contrast, in Poland, Korea, Japan, and Australia there has been more impact from digital-born brands.

ONLINE REACH OF NEWSPAPERS, BROADCASTERS AND DIGITAL BORN BRANDS (SELECTED COUNTRIES)

| Broadcasters | Digital-born | ||

|---|---|---|---|

| USA | 63% | 48% | 59% |

| Canada | 60% | 51% | 52% |

| UK | 59% | 46% | 31% |

| Germany | 49% | 53% | 47% |

| France | 43% | 57% | 40% |

| Spain | 62% | 75% | 63% |

| Finland | 62% | 85% | 33% |

| Poland | 70% | 71% | 87% |

| Korea | 71% | 55% | 87% |

| Japan | 56% | 40% | 63% |

| Australia | 47% | 62% | 64% |

Base: Total sample in each country

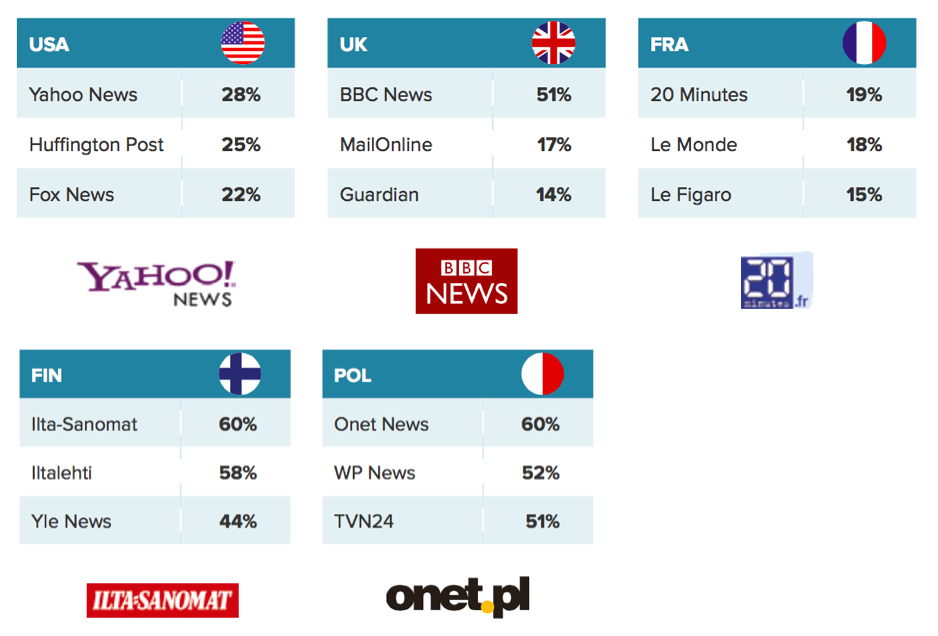

Looking in more detail at some of these countries, we can understand more about what is driving these differences. The US has a number of strong national broadcast brands like Fox and CNN, while newspapers tended to have a local footprint which has made it harder to develop online readership across the country. At the same time, the entrepreneurial culture in the US has spawned a huge number of digital-born start-ups, from Yahoo and AOL to newer brands that together reach almost two-thirds (59%) of our sample. The UK has a national broadcaster (the BBC), which invested early in digital, and a highly competitive newspaper sector, which has also gained strength from accessing other English-speaking markets. By contrast, in France, we see a more fragmented picture with traditional newspaper brands like Le Monde and Le Figaro key online destinations but also with a strong digital-born sector which includes US imports like Yahoo and the Huffington Post as well as profitable journalistic start-ups like Mediapart. In Finland, the strong reading tradition along with a history of newspaper subscription has helped established print brands to reach over four-fifths of our sample online (85%), a significant proportion of whom pay for online news. The public broadcaster YLE also cuts through online, though mainly with older groups, but there has been little progress for digital-born media. Finally in Poland, we see heavy use of local portals like Onet and WP, which mainly aggregate news in addition to broadcast and newspaper groups.

Scroll data area to see more

TOP NEWS BRANDS ONLINE (SELECTED COUNTRIES)

Base: Total sample in each country

Digital-born sector is increasingly complex and fragmented

The digital-born sector is increasingly difficult to categorise. In the past we have made a distinction between ‘first-wave’ digital brands that primarily aggregate news from multiple sources and newer ‘second-wave’ companies that produce their own content such as the Huffington Post and BuzzFeed. But these distinctions are by no means clear and differ by country and region.

Amongst ‘first-wave’ aggregators we can see brands like Yahoo, MSN, and AOL, which became popular by bundling email or search services via desktop, increasingly struggling to make money and remain relevant. Many have been hit hard by the downturn in display advertising and the move to mobile. By contrast some non-English-speaking national aggregators seem to be going from strength to strength, with many diversifying into original news content, video, and entertainment.

Naver is South Korea’s biggest web portal and search engine that started life as an offshoot of Samsung’s IT department. In our survey it is used as a source of news by 66% of our Korean respondents. Its newsstand aggregates content from all the major Korean publishers but most of its money is made elsewhere. Unlike some Western portals, advertising revenues remain strong.

Formed as a joint venture between Yahoo US and internet company SoftBank, Yahoo Japan is the most popular web portal and search engine in Japan. Well over half of our sample (59%) use its news service weekly as it provides easy access to a range of Japanese publishers. Facing new threats from mobile aggregators like SmartNews, it is stepping up original news production and investing more in video and entertainment.

Sapo is a Portuguese portal that also started life as a search engine but has expanded into email and web hosting following an acquisition by Portugal Telecom. It produces its own news content but also acts as a platform for the wider news industry. It has deals with most top media organisations that allow them to republish news through the Sapo website. In our survey 36% of our online sample use the main portal with many more accessing branded areas of the site.

Mynet is Turkey’s most popular web portal offering news, sport, finance, games, entertainment, and social media. It built its business by offering free email to Turkey’s large population, which has helped it attract a large audience who come back every day. In our survey 36% use Mynet as a gateway or destination for news weekly.

Seznam is a Czech web portal and search engine which has a popular news section, visited by three-quarters (74%) of respondents to our survey in a given week. Seznam links to partner websites such as Novinky.cz, Sport.cz, and Super.cz.

By accident or design, many of these national portals have become – and remain – important gateways to news. But like Facebook and Apple many have ambitions to be platforms and destinations in their own right. Through bundling and deal making they have forged a powerful position. It remains to be seen how well they survive the next wave of competition from new mobile first aggregators, social networks, and chat apps.

Second-Wave Content Producers

In recent years, a second wave of news companies has emerged that are focused on producing original content alongside business models that do not primarily rely on display advertising. Again this is a complex area to categorise, but we can subdivide these into brands that are focusing on global scale with income from advertising or increasingly from sponsored content, and those focusing on national niches and subscription models.

In the first category, our data show that the most successful companies in terms of reach have been BuzzFeed and the Huffington Post. Both have focused on distributing content through social media but are also building up destination websites and apps – along with a news voice of their own.

BuzzFeed has hired new staff and high-profile journalists in a number of countries including the UK and Australia, working on subjects like politics and the environment. It has also launched a new service in Japan this year. Everywhere, it has focused relentlessly on millennial audiences and is most popular with 18–24s. It has been developing new video formats including a number of non-news channels and in business terms makes money by selling its expertise in distributed content to commercial brands, though doubts have been raised about the scalability of this approach. 1

The Huffington Post has focused on partnerships with traditional news providers such as Le Monde in France, L’Espresso group in Italy, and El Pais in Spain and is increasingly looking to share content across countries. [91. http://reutersinstitute.politics.ox.ac.uk/people/jimmy-maymann It is also refocusing its activities on video and sponsored content.

Both the Huffington Post and BuzzFeed have greatest reach in English-speaking countries, though both have made gains in other countries including France and Brazil over the past year.

Vice News operates in 24 countries – though locally produced content remains limited in most. It reaches only a small section of internet news users in most countries but twice as many under-35s.

Scroll data area to see more

SELECTED DIGITAL-BORN BRANDS WEEKLY NEWS REACH, COMPARED WITH SELECTED TRADITIONAL BRANDS

| Huffington Post | BuzzFeed | Vice | BBC | CNN | New York Times | |

|---|---|---|---|---|---|---|

| USA | 25% | 16% | 4% | 10% | 21% | 14% |

| UK | 14% | 9% | 2% | 51% | 2% | 2% |

| France | 13%* | 4% | 2% | 3% | 2% | 2% |

| Germany | 8%* | 2% | 1% | 4% | 3% | 2% |

| Spain | 8%* | 3% | 3% | 6% | 7% | – |

| Italy | 12%* | 2% | 2% | 8% | 6% | 3% |

| Greece | 13%* | 4% | 7% | 15% | 11% | – |

| Ireland | 11% | 10% | 2% | 22% | 6% | 5% |

| Australia | 10% | 10% | 2% | 14% | 8% | 4% |

| Canada | 19% | 13% | 4% | 9% | 15% | 6% |

| Japan | 5%* | 2% | – | 4% | 6% | 2% |

| Weighted average (24 countries) | 11% | 6% | 2% | 8% | 8% | 5% |

Base: Total sample in each country.

Note: Weighted percentage calculated using population data from Internet World Stats and the World Bank: weighted = (country population x percentage adults x percentage accessed)/total population of all countries surveyed. Brazil and Turkey are not included in weighting due to the absence of reliable data about its urban population.

*Joint ventures or former joint ventures

Journalistically Led News Brands

In our second sub-category – and particularly in European markets – we see a number of journalistically led news brands that have emerged to become profitable based on donations or subscription models.

De Correspondent is a Dutch journalism platform that focuses on analysis and investigative reporting. In 2013 it raised around $1.7m in voluntary contributions for a site focusing on in-depth news. The site is ad-free and currently has over 40,000 members or subscribers, though content can be freely shared in social media. It reaches just 1% of respondents to our survey and 3% of under-35s.

Mediapart is a French online investigative and opinion journal created in 2008 by a former editor of Le Monde. It has become an important part of the French media landscape with 118,000 paying subscribers and 8% weekly reach in our survey. Mediapart employs over 60 staff with a turnover of around €10m. [92. https://blogs.mediapart.fr/edition/les-invites-de-mediapart/article/160316/building-independence

El Confidencial is one of several digital-born publications in Spain enjoying success with quality journalism. In our survey the site is the fifth most popular in Spain with 20% weekly reach. It employs over 100 staff, and is profitable, with most income from advertising. Journalistic redundancies from the traditional sector have fuelled a number of other Spanish start-ups such as El Español, which launched last year having raised €3.6m through crowdfunding and offers free content as well as a monthly subscription model.

Given the vast range of approaches, it is hard to draw broad conclusions about the digital-born market. The majority of start-ups, however, employ relatively few journalists and tend to cover a subset of the news landscape. Some focus on serving specific niches, whilst others focus on the lighter or fun side of news or provide a different take or voice on the news. They are also not immune to the rise of platforms and the move to mobile, trends which are making it harder for all publishers to build sustainable business models.

Digital-born brands have certainly added to the plurality of many media markets but they are a long way from replacing traditional media in providing comprehensive coverage on a wide range of stories as well as consistent in-depth journalism across the waterfront.